- Markets in January

- The economic picture

- Global market indices

- Commodity sector news

- Currencies

- Cryptocurrencies

- Fixed Income

- What to think about in February

- Key events in February

Markets in January

Equities markets were largely in positive territory in January as investors focused on the US economy’s continued strong growth. The release of DeepSeek-R1, a cost-effective generative AI model from China, triggered a significant market reaction on 27th January, with investors reassessing their assumptions about the future of artificial intelligence. Shares of Nvidia, a leading provider of graphics processing units crucial for AI development, fell by 17%. Similarly, companies involved in nuclear power, data centers, and other infrastructure components experienced substantial declines. The S&P 500 is +2.68% MTD, the Dow is +5.42% MTD, while the Nasdaq 100 is +2.15% MTD. The NYSE is +1.67% MTD. European equity markets have also been positive in January, with the STOXX 600 +5.25% MTD.

In the bond market, yields were volatile as uncertainty about tariffs rose in the US and the UK following on from the US election and the UK budget. Investors appear to be defensive in their portfolios due to uncertainties around the Trump administration's policies, particularly in relation to tariffs, and their possible impact on yields and the USD. In addition, investors are leery of the rising US debt and proposed changes in US tax policies that may exacerbate debt levels. The Trump presidency with Republican majorities in the Senate and House brought the spectre of tariffs and rising inflation to the fore. Markets reacted positively to Trump’s suggested nominee for Treasury secretary, Scott Bessent, who currently runs macro hedge fund Key Square Group, on the belief that he may have a more gradualist approach to tariffs. It is hoped by many investors that he may be a more moderating force in the cabinet relative to other cabinet nominees including Jamieson Greer, US trade representative, Kevin Hassett, director of the National Economic Council, Howard Lutnick for Commerce secretary, Marco Rubio, Secretary of State, and Michael Waltz, as national security adviser.

The economic picture

The dollar index was volatile in January due to uncertainty around Trump’s tariff, but was very badly hit by the drop in tech stocks, particularly in Nvidia shares, on 27th January. However, there has been some recovery since and the index is -0.50% MTD. The dollar had been rallying on expectations that President Donald Trump will increase tariffs on the US’ main trading partners, thereby pushing inflation upwards and limiting the Federal Reserve’s ability to cut interest rates. The US labour market continues to show strength with the December nonfarm payrolls at 256,000, up from 227,000 in November. Inflation was down in December, with headline inflation rising 2.9% in December compared with the same month last year, up from November’s 2.7% rate. On a monthly basis, the CPI rose 0.4% in December compared with 0.3% in November. Core CPI, which excludes volatile food and energy prices, rose 2.6% on an annual basis and 0.2% on a monthly basis, compared with 0.3% in November.

On the growth front the US continues to show strength but with growth moderating. The Flash Composite PMI in January came in at 52.4, down from December’s 55.4 and a 9-month low. The Flash Services PMI was also down, coming in at 52.8 from December’s 56.8 and also a 9-month low. The Flash Manufacturing PMI came in at a 7-month high at 50.1, up from December’s 49.4. However, consumers are feeling less confident. The Conference Board's consumer confidence index declined by 5.4 points in January to 104.1. December's reading was revised up by 4.8 points to 109.5 but was still down 3.3 points from the previous month. The Present Situation Index—based on consumers’ assessment of current business and labor market conditions—fell sharply in January, dropping 9.7 points to 134.3. The Expectations Index—based on consumers’ short-term outlook for income, business, and labor market conditions—fell 2.6 points to 83.9, but remained above the threshold of 80 that usually signals a recession ahead. The University of Michigan consumer sentiment survey in January fell to a three-month low of 71.1 from 74 in December, largely due to growing concerns about unemployment and the potential inflationary effects of upcoming tariffs. Long-term inflation expectations rose to 3.2% from 3% in December, while short-term expectations increased to 3.3%, the highest level since May.

In the eurozone, markets are fully expecting a further 25 bps cut at today’s meeting. Eurozone inflation rose 2.4% from a year ago in December, up from 2.2% in November. Core inflation, excluding volatile items such as food, energy, alcohol, and tobacco, stood at 2.7%. Services inflation came in at 4.0%. On the growth front, the eurozone Flash Composite PMI exceeded expectations with the HCOB Flash Composite PMI rising to 50.2, surpassing the expected 49.7, and up from December’s 49.6. However, the manufacturing sector remained in contraction for the 31st consecutive month coming in at 46.1. This was still better than December’s 45.1 and an 8-month high. The service sector came in at 51.4, down from December’s 51.6. In addition, Germany, Europe’s largest economy, is still experiencing weak growth with Q4 GDP falling 0.2%, more than forecast and supporting recession fears. Markets also remain worried by the possible trade tariffs from the Trump administration as well as about the 23 February election in Germany. As noted by the Financial Times, support for the governing coalition, which includes Chancellor Olaf Scholz’s Social Democrats (SPD), the Greens and the pro-business Free Democrats (FDP), has fallen considerably. And, with center-left Chancellor Olaf Scholz declaring that he “can’t trust” conservative leader Friedrich Merz of the CDU after the Bundestag narrowly approved, with the support from the far-right Alternative for Germany (AfD) , a nonbinding motion to allow asylum-seekers to be turned back at the border, there is more of a chance of the CDU/CSU forming a coalition with either the Greens or the SPD.

In the UK there is growing concern over the country’s ability to service its debt. Inflation is still not in line with the BoE’s target rate of 2% but is slowing. The headline rate rose by 2.5% in the 12 months to December 2024, only slightly below November’s 2.6%. Core inflation, which strips out volatile food, energy, and alcohol inputs, also rose by less than expected. The measure rose 3.2% on the year, below forecasts, and down from 3.5% in November. This did provide some relief to the Treasury and may have given some room for the Bank of England to cut rates at its first meeting of the year on 6 February. However, according to the BoE, headline inflation is expected to increase to around 2.75% by the second half of 2025 as weakness in energy prices falls out of the annual comparison, which will likely reveal the continuing persistence of domestic inflationary pressures. One of the chief concerns for markets is that the growth picture for the UK is not promising. The S&P Global Composite PMI, although rising from 50.4 in December to a three-month high of 50.9 in January, has, according to S&P, now been at such a low level as to signal zero GDP growth for three successive months. The survey suggested that a loss of confidence was driven partly by the payroll tax increase on businesses announced in the 30 October budget. Firms’ expectations for activity in the year ahead were the most pessimistic since late 2022. The Flash Services PMI also dropped to 50.0, down from October’s 52.0 and also a 13-month low. The Flash Manufacturing PMI continued to fall and reached a 9-month low, hitting 48.6 and down from October’s 49.9. In addition, consumer confidence is down with the GfK Consumer Confidence Index for January falling by five points to -22 in January. Consumer expectations for the economy over the next 12 months fell by eight points to minus 34, the worst in almost two years.

BoE policymakers are likely to be concerned that labour market data continues to show inflationary pressures despite a weakening job market. According to the Office for National Statistics, pay excluding bonuses rose 5.6% in the three months through November from a year earlier, up from 5.2% the previous month. It was strongest in six months and slightly above the 5.5% expected by economists. Private-sector pay growth also accelerated, rising to 6% from 5.5% in the three months through September. However, employment is falling, with unemployment edging up to 4.4% in the three months through November, from 4.3% in the three months through October. The number of employees on payroll also hit the lowest level in over a year after falling by 47,000 in December. This was the largest drop since the end of 2020.

Global market indices

US:

S&P 500 +2.68% MTD

Nasdaq 100 +2.15% MTD

Dow Jones Industrial Average +5.42% MTD

NYSE Composite +1.67% MTD

The Equally Weighted version of the S&P 500 posted a +3.14% this month, 0.46 percentage points higher than the benchmark.

The S&P 500 Communication Services sector is the top performer this month at +6.95% MTD, while Information Technology underperformed at -1.62% MTD.

On Wednesday US equities experienced a broad decline, with the S&P 500 decreasing by 0.5%, the Nasdaq 100 falling by 0.2%, and the Dow Jones Industrial Average slipping 0.3%, or 137 points. The technology sector experienced a downturn due to increased volatility, driven by concerns that DeepSeek, a Chinese startup, had developed a cost-effective AI model that could disrupt the valuations of established tech companies.

This development has exacerbated anxieties on Wall Street, where market concentration within the S&P 500 has reached a 20-year high, with a disproportionate reliance on the performance of a few tech giants.

Despite the recent market correction, investor exposure to the tech sector remains significant. Following the market close, investors analysed earnings reports from Meta Platforms, Microsoft, Tesla, and other companies. Investor scrutiny is anticipated to be heightened due to the questions surrounding artificial intelligence prompted by DeepSeek's emergence.

In Europe, ASML reported stronger-than-expected order numbers for Q4 of 2024, providing positive news for AI bulls.

In corporate news, representatives from Hewlett Packard Enterprise met with US antitrust officials on Tuesday regarding its proposed $14 billion acquisition of Juniper Networks, according to sources familiar with the matter.

Apple has been developing support for the Starlink network in its latest iPhone software in collaboration with SpaceX and T-Mobile. This would provide an alternative to Apple's own satellite communication service.

Nasdaq CEO Adena Friedman anticipates a robust environment for IPOs in Q2 and the remainder of 2025, as investor confidence grows with stabilising interest rates and inflation.

Alibaba Group released benchmark scores and highlighted the purported world-leading performance of its newly released AI model.

T-Mobile US reported Q4 2024 results that exceeded analysts' forecasts, driven by continued growth in wireless subscribers and home internet customers.

Europe:

Stoxx 600 +5.25% MTD

DAX +8.68% MTD

CAC 40 +6.66% MTD

FTSE 100 +4.71% MTD

IBEX 35 +5.96% MTD

FTSE MIB +6.39% MTD

In Europe, the Equally Weighted version of the Stoxx 600 is +4.14% in January, 1.11 percentage points lower than the benchmark.

The Stoxx 600 Banks is the leading sector this month, up +9.67% MTD, while Utilities has exhibited the weakest performance at -0.12% MTD.

Global:

MSCI World Index +3.25% MTD

Hang Seng +0.82% MTD

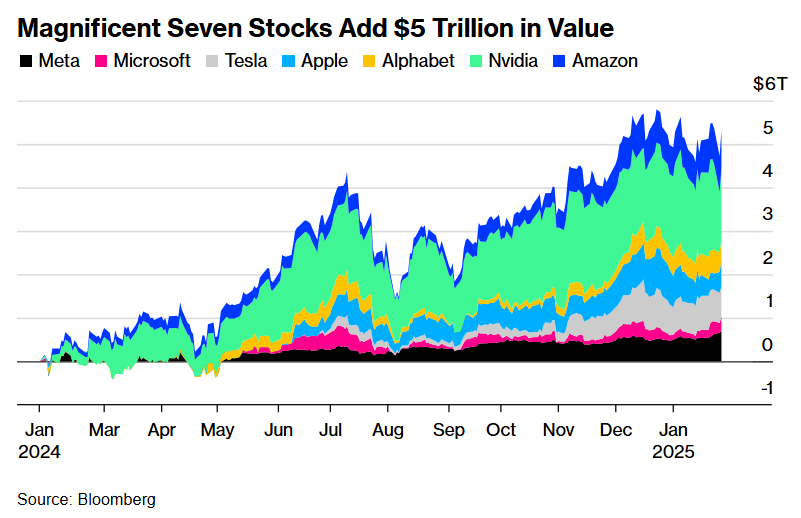

Mega cap stocks had a mixed performance in January with Alphabet +3.23%, Amazon +8.06%, Meta Platforms +15.54%, Microsoft +4.94%, while Apple -4.42%, Nvidia -7.89%, and Tesla -3.65%.

Meta Platforms Q4 earnings. Meta Platforms exceeded expectations in Q4 2024, reporting record revenue driven by advancements in AI within its advertising sector.

The parent company of Facebook and Instagram reported EPS of $8.02, significantly surpassing the FactSet analyst consensus estimate of $6.76. Revenue reached $48.4 billion, exceeding projections of $47 billion. Meta attributed this success to AI-driven enhancements in its advertising business and anticipates Q1 2025 growth between 8% and 15%. Net income also surpassed expectations, reaching $20.8 billion.

Following the earnings release and recent announcements regarding increased investment in AI, Meta's shares experienced an increase of 2.3% in after-hours trading on Wednesday. The company's CapEx estimate for 2025 is approximately 70% higher than 2024 projections, between $60 billion and $65 billion, with a significant portion dedicated to the construction of a massive data center in Louisiana. CEO Mark Zuckerberg described the facility's scale, stating it would cover a substantial portion of Manhattan. Furthermore, Meta anticipates its GPU count will exceed 1.3 million by year-end. See report.

Microsoft Q4 earnings. Microsoft’s share price was down 5% in after-hours trading following the company's announcement of a growth deceleration in its Azure cloud computing division during Q4 2024. Despite this slowdown, Microsoft exceeded overall financial expectations. Revenue increased by 12% to $69.6 billion, and net income rose by 10% to $24.1 billion, surpassing analyst projections.

Azure revenue growth reached 31% in Q4, meeting the lower end of the company's guidance but falling slightly short of the 32% growth anticipated by analysts, according to FactSet. Microsoft attributed this moderation to constraints in data center capacity, hindering its ability to fully capitalise on surging demand from artificial intelligence companies.

Microsoft highlighted the robust performance of its AI-related businesses, with annualised revenue exceeding $13 billion. The company reported EPS of $3.23, surpassing analyst estimates of $3.11. FactSet compiled consensus forecasts had projected net income of $23.3 billion and revenue of $68.9 billion. In Q4 2023, Microsoft reported EPS of $2.93, net income of $21.9 billion, and revenue of $62 billion. See report.

Tesla Q4 earnings. Tesla’s share price rose by 4.7% following the release of the company's Q4 earnings report. Tesla reported adjusted net income of $2.57 billion, or $0.73 EPS, slightly below analyst expectations. The company's overall net income decreased by 71% compared to the same period last year, partially due to a substantial one-time tax benefit recorded in the prior-year quarter. Despite this, revenue for the quarter reached $25.7 billion, a modest increase from the $25.2 billion generated in the comparable period of the previous year.

Tesla's energy storage business, which encompasses both residential and industrial battery solutions, exhibited robust growth. Revenue in this segment more than doubled to $3 billion during the fourth quarter, effectively mitigating the impact of reduced selling prices for several of the company's core vehicle models. Furthermore, revenue recognised from the sale of regulatory credits amounted to $692 million, representing a nearly 60% increase y/o/y.

This strong performance in the energy storage sector and regulatory credit sales contributed to Tesla's positive share price movement despite the slight miss on earnings expectations. See report.

Energy stocks experienced a positive performance this month, with the Energy sector +4.33% MTD. Energy Fuels +8.93%, Marathon Petroleum +8.52%, Chevron +7.49%, Phillips 66 +7.22%, Baker Hughes Company +5.00%, Shell +4.81%, ConocoPhillips +2.41%, ExxonMobil +1.02%, and Apa Corp +0.39%, while Occidental Petroleum -1.17%, and Halliburton -3.02%.

Materials and Mining stocks had a positive performance this month. The Materials sector is +5.24% MTD. Gold is +5.32% MTD, while silver prices are +7.98% MTD and copper prices are +6.81% MTD. Mosaic +16.68%, Yara International +12.67%, Newmont Mining +11.74%, Sibanye Stillwater +9.88%, Nucor Corporation +8.71%, Celanese Corporation +2.50%, and Albemarle +0.23%, while Freeport-McMoRan -4.73%.

Commodities

Gold is +5.32% MTD. Gold prices declined -0.15% on Wednesday as the US dollar and bond yields strengthened following the Fed's widely anticipated decision to maintain interest rates.

The Fed's decision to hold rates steady provided little indication of when further decreases in borrowing costs might occur, given the current economic landscape characterised by above-target inflation, continued growth, and a low unemployment rate. This decision was largely expected after three consecutive rate cuts in 2024, which collectively lowered the Fed's benchmark rate by one full percentage point.

Investors expect that the central bank will not cut rates again until June, according to short-term interest rate futures after the statement's release.

Fed Chairman Jerome Powell commented that it is premature to assess the impact of the US President's policies and that the Fed will carefully evaluate the implications of the new governmental policy regime.

Oil prices have had a positive performance in January with WTI +1.86% MTD and Brent +1.73% MTD. This was largely due to US sanctions on Russia squeezing supply and forcing Indian and Chinese refiners to look elsewhere.

Oil prices declined on Wednesday, with the US benchmark settling at its lowest point this year, following a larger-than-anticipated increase in domestic crude stockpiles within the world's leading petroleum producer and consumer.

Brent crude futures closed down 69 cents, or -0.89%, at $76.94 per barrel. US crude futures fell $1.01, or -1.37%, to $72.91, marking their lowest settlement price of the year thus far.

The White House reiterated on Tuesday the US President's intention to implement 25% tariffs on imports from Canada and Mexico beginning 1st February. Near-term oil trade is expected to remain volatile as investors assess the potential impact of tariff threats, sanctions on Russian energy supplies, and concerns regarding economic growth in major consuming nations.

Traders are now focused on the upcoming OPEC+ ministerial meeting scheduled for 3rd February, where discussions regarding the group's plans to increase supply from April will be central.

Concerns about supply have lessened following an announcement from Libya's National Oil Corporation on Tuesday that export operations have resumed normal activity after discussions with protestors who had demanded a halt to loadings at a key national oil port.

EIA reports crude stock increase, refinery utilisation drop, and distillate drawdown. US crude oil inventories increased last week due to reduced refinery utilisation, the Energy Information Administration (EIA) reported Wednesday. Winter storms across the US impacted refinery operations and simultaneously increased demand for distillates.

Crude inventories rose by 3.5 million barrels to a total of 415.1 million barrels during the week ending 24th January, according to the EIA. At the Cushing, Oklahoma, delivery hub, crude stocks increased by 326,000 barrels, reaching 21 million barrels.

Total US product demand averaged 20.29 million barrels per day (bpd) over the past four weeks, a 2.5% increase compared to the same period last year. Refinery crude runs decreased by 333,000 bpd during the week, the EIA noted, with utilisation rates falling 2.4 percentage points to 83.5%.

Distillate stockpiles, including diesel and heating oil, declined by 5 million barrels to 124 million barrels, representing their largest weekly decrease since March 2022, EIA data revealed. Distillate fuel oil supplied, a proxy for demand, rose to 4.51 million bpd last week, up from 4.11 million bpd the previous week, reaching its highest level since March 2022.

Distillate inventories in the Midwest, however, reached their highest point since January 2024. US gasoline stocks also increased, rising by 3 million barrels to 248.9 million barrels.

Finally, net US crude imports increased by 532,000 bpd last week, the EIA reported, reaching 2.76 million bpd. Conversely, weekly crude exports fell by 829,000 bpd to 3.69 million bpd.

Currencies

The dollar had a choppy January due to volatile yields associated with the expectations that the new Trump administration would impose tariffs that will result in higher inflation. The dollar index has retreated over the month; it is -0.50% MTD. The GBP is -0.53% MTD against the USD. The EUR is +0.64% MTD against the USD.

The US dollar strengthened against major currencies on Wednesday following the Fed's widely anticipated decision to maintain interest rates. The Fed's accompanying statement offered little indication regarding further reductions in borrowing costs this year.

FOMC members unanimously voted to hold the overnight interest rate steady within the current 4.25% - 4.50% range. This decision places the Fed in a holding pattern as it awaits further data on inflation and employment, as well as greater clarity on the economic impact of the US President's policies. During his press conference, Fed Chairman Jerome Powell stated that it is premature to assess the effects of the President's policies and affirmed that the central bank's 2% inflation target remains unchanged.

The euro declined -0.07% to $1.0421. Eurozone bank lending to businesses increased last month, suggesting that recent interest rate reductions are beginning to impact the real economy, according to data released by the ECB.

Against the Japanese yen, the dollar weakened slightly by -0.23% to ¥155.18.

The dollar index, a measure of the dollar’s strength against a basket of currencies including both the euro and the yen, edged down -0.06% to 107.85 in afternoon trading. The index reached a one-month low of 106.96 on Monday. However, the index remains over 4% higher than it was before the US election in November.

The British pound appreciated slightly against the dollar on Wednesday, rising +0.10% to $1.2449. The pound weakened against both the dollar and the euro earlier in January due to growing concerns regarding the UK’s economic outlook amid a global bond selloff. However, some pressure on the British government has subsided as yields on UK gilts have retreated from recent highs.

The pound also strengthened slightly against the euro for a fifth consecutive day, with one euro at 83.76 pence.

While investors have increased their bets on BoE rate cuts this year, with 71 bps of easing currently priced in, they still anticipate less aggressive easing from the BoE compared to the ECB, where markets are forecasting 90 bps of rate reductions.

Cryptocurrencies

Bitcoin +11.04% MTD to $103,634.

Ethereum -5.97%MTD to $3,134.70.

Bitcoin was up +2.42% on Wednesday despite the Fed keeping rates at the 4.25-4.50% range. Fed Chair Jerome Powell said banks are “perfectly able to serve crypto customers as long as they understand and can manage the risks” and added that “a greater regulatory apparatus around crypto” from Congress would be “very constructive.” Ethereum was +2.08% on Wednesday.

Bitcoin hit a record $109,241 ahead of Trump’s inauguration on 20 January, but subsequently slid back. Nevertheless, it is up over 50% since his election victory. Cryptocurrencies have generally been up in January on signs that the new Trump administration is going to honour its campaign promises around easing cryptocurrency regulation. The new Securities and Exchange Commission (SEC) Acting Chairman Mark T. Uyeda has announced the formation of a new crypto task force which aims to develop a comprehensive and clear regulatory framework for crypto assets. Meanwhile President Trump signed an executive order promoting US leadership in blockchain and digital assets including cryptocurrency. The executive order outlines policies to ensure access to open public blockchain networks for lawful purposes, promote lawful dollar-backed stablecoins, ensure fair access to banking services, and provide regulatory clarity with technology-neutral regulations. It also prohibited the use of CBDCs in the US. Trump also set up a new working group within the National Economic Council (NEC) to propose a federal regulatory framework for digital assets. It is chaired by David Sacks, the special advisor for artificial intelligence (AI) and crypto and includes the secretary of the treasury, US attorney general and chair of the SEC.

Note: As of 5:45 pm EST 29 January 2025

Fixed Income

US 10-year yield -3.2 basis points MTD to 4.544%.

German 10-year yield +21.4 basis points MTD to 2.583%.

UK 10-year yield +6.1 basis points MTD to 4.629%.

US Treasury 10-year bond yields are -3.2 basis points (bps) over the past month.

On Thursday the Fed kept rates at the 4.25 - 4.50% range. In its updated statement, the Fed omitted language indicating that inflation ‘has made progress’ toward the 2% target, instead stating that the pace of price increases ‘remains elevated.’ This revision reflects the Fed's recognition that inflation continues to exceed its target and may be stabilising at a higher-than-desired level.

During the subsequent press conference, Powell emphasised the Fed’s commitment to achieving further reductions in inflation. He noted that a pathway for continued progress remains visible, citing the steady decline in shelter inflation as one example.

Powell also clarified that the Fed does not require inflation to reach its 2% annual target before considering interest rate cuts. The CME's FedWatch Tool gives an 18% probability of a 25 bps cut at the FOMC meeting ending on 19th March. Traders are now pricing in only 46 bps of cuts this year; prior to the Fed’s statement, they were pricing in 48 bps.

The benchmark German 10-year yield is +21.4 bps in January at 2.583%, while the UK 10-year yield is +6.1 bps at 4.629%. The spread between US 10-year Treasuries and German Bunds decreased by 12.2 bps from 208.3 bps at the end of December to 196.1 bps now.

Italian bond yields, a benchmark for the eurozone periphery, are +12.4 bps this month to 3.654%. Consequently, the spread between Italian and German 10-year yields widened slightly by 0.7 bps this month to 107.1 bps from 106.4 bps at the end of December.

US Treasury yields reversed their earlier gains on Wednesday following remarks from Fed Chair Jerome Powell, who expressed expectations for continued progress on inflation. This came despite the Fed's decision to remove language from its latest policy statement that had previously acknowledged easing inflation.

During the subsequent press conference, Powell emphasised the Fed’s commitment to achieving further reductions in inflation. He noted that a pathway for continued progress remains visible, citing the steady decline in shelter inflation as one example. Powell also clarified that the Fed does not require inflation to reach its 2% annual target before considering interest rate cuts. Powell further stated that the Fed still has room to continue reducing the size of its balance sheet, asserting that banking system reserves remain ‘abundant’ and that the Fed retains firm control over the fed funds rate.

The yield on the two-year US Treasury note, which is highly sensitive to Fed fund rate expectations, rose by +2.1 bps to 4.226% on the day, having reached as high as 4.263% following the Fed’s statement. The yield on the 10-year US Treasury note increased by +0.6 bps to 4.544%, after reaching an earlier high of 4.593%.

In the eurozone, bond yields remained relatively unchanged on Wednesday, as investors paused ahead of the FOMC meeting and the ECB policy decision scheduled for today.

Germany’s 10-year bond yield rose by +1.9 basis points to 2.583%, placing it within the midpoint of its recent range. The ECB is widely anticipated to implement a 25 bps rate cut on Thursday in an effort to stimulate the sluggish European economy.

Economic data released on Wednesday indicated that bank lending to businesses across the 20-nation eurozone increased last month, suggesting that recent rapid interest rate cuts are beginning to impact the broader economy.

Germany’s two-year yield, which is particularly sensitive to interest rate changes, remained flat at 2.263%. Meanwhile, Italy’s 10-year bond yield increased by +1.6 bps to 3.654%.

French bond spreads remained largely unchanged despite reports that budget negotiations in France were on the verge of collapse. This development followed the withdrawal of Socialist Party officials from discussions, raising concerns over fiscal policy stability.

The spread between French and German 10-year bond yields stood at 73.7 bps, nearing its tightest level since mid-November. The ongoing political uncertainty in Germany and France, coupled with the potential risk of a trade conflict with the US that could dampen economic growth and drive fixed-income rallies, is contributing to continued volatility in European bond markets.

In the near term, European bond spreads are expected to remain volatile due to the uncertain political landscape in major economies such as Germany and France, as well as broader macroeconomic risks.

Note: Data as of 5:00 pm EST 29 January 2024

What to think about in February 2025

The focus for markets has been on whether President Trump will go through with his threatened tariffs or if they are only opening “negotiation tactics” with countries that have a trade imbalance with the US.

Fed maintains benchmark rate, in ‘wait-and-see’ pause. As widely anticipated, the FOMC concluded its January meeting with no adjustments to the fed funds rate, which remains at 4.25% - 4.50%. The accompanying statement underwent minor revisions, now characterising labour market conditions as ‘remaining solid’ (previously ‘generally eased’) and inflation as ‘remaining somewhat elevated’ (previously ‘has made progress toward the Committee's 2% objective’).

Market focus leading up to the meeting had centered on the potential inflationary impact of US administration policies, with a rate hold considered a near certainty. Initial interpretations of the statement suggest a hawkish stance, though Fed Chair Jerome Powell struck a more dovish tone during the press conference. Powell acknowledged the wide range of potential effects stemming from tariffs and reiterated the Fed's data-dependent approach, emphasising that they are ‘not in a hurry.’

Current market expectations, as reflected by the CME FedWatch Tool, indicate a roughly 82% probability of another rate hold at the March meeting. Analysts anticipate an extended pause in rate hikes until greater clarity emerges regarding both Trump administration policies and inflationary trends.

Essentially, the Fed is navigating a landscape of considerable uncertainty, aiming to respond effectively to incoming data and evolving policy developments. In this environment, particularly with significant uncertainty surrounding tariff policy, the Fed's forecasting ability is limited. Maintaining the current policy stance until a clearer picture emerges is a sensible strategy.

However, should the coming months reveal a continued softening of inflation coupled with a slight moderation in job growth, a renewed dovish shift in Fed communications may be expected.

DeepSeek-R1 forces a reassessment of AI's infrastructure and innovation. The release of DeepSeek-R1, a cost-effective generative AI model from China, challenges two prevailing narratives: the dependence of AI development on resource-intensive infrastructure and the dominance of American technology companies in the AI landscape.

The market downturn was primarily driven by concerns about the potential impact of DeepSeek-R1 on the demand for AI-related hardware and infrastructure. This sell-off raises important questions about the balance between fundamental shifts and investor sentiment in driving market behavior. While the magnitude of the decline suggests a reassessment of the fundamental outlook for AI infrastructure, it is also evident that investor enthusiasm for AI had reached elevated levels, potentially creating a vulnerability to negative news.

DeepSeek-R1, developed by a team led by hedge fund manager Liang Wenfeng, claims to achieve comparable performance to leading AI models while requiring significantly lower training and operational costs. This has prompted concerns about reduced demand for expensive hardware and energy-intensive data centers.

However, it is crucial to avoid premature conclusions. The AI landscape is still evolving, and the long-term implications of DeepSeek-R1 remain uncertain. While the model's efficiency may reduce the intensity of resource consumption, broader adoption of AI could ultimately increase overall demand for infrastructure.

Furthermore, the value creation within the AI ecosystem is likely to shift over time. Analogous to the development of the internet, value may eventually migrate from the infrastructure providers towards those who leverage AI for various applications.

The upcoming fourth-quarter earnings season will likely provide additional insights into the impact of DeepSeek-R1, the capital expenditure plans of major technology companies, and the progress towards monetising AI technologies. Investors should exercise caution and avoid overreacting to short-term market fluctuations while continuing to monitor these developments closely.

Key events in February 2025

The potential policy and geopolitical risks for investors that could negatively affect corporate earnings, stock market performance, currency valuations, sovereign and corporate bond markets and cryptocurrencies include:

3 February Bank of Japan Monetary Policy Meeting. After the BoJ raised its target rate by a quarter point to 0.5%, the highest since 2008, at its January meeting, it suggested that there will be more rate cuts this year. However, the BoJ is likely to take a wait and see approach to potential US tariffs and the impact on demand as well as global currencies.

6 February Bank of England Monetary Policy Meeting. The BoE may surprise markets and raise rates again this month based on signs of weak growth. However, with wage inflation well above target and headline inflation due to rise later this year, this is unlikely. The BoE will likely keep the door open to further rate cuts this year, but may slow the pace of cuts. February's MPC meeting will be accompanied by the publication of a new Monetary Policy Report. This could well contain further information about what the Bank of England expects to happen this year and will lay out the projected path for rates policy.

10 - 11 February AI Action Summit, Paris, France. The third summit of its kind will focus on public interest AI; the future of work; innovation and culture; trust in AI; and global AI governance.

14-16 February Munich Security Conference, Germany. The conference will focus on global security challenges, including global governance, democratic resilience, climate security, the state of the international order as well as regional conflicts and crises. The future of the transatlantic partnership will also be a focus and the conference will end with discussions on Europe’s role in the world.

20-21 February G20 Foreign Ministers meeting, Johannesburg, South Africa. The meeting will likely be dominated by discussions over ongoing geopolitical conflicts such as Ukraine and the situation in Syria.

23 February Federal Elections Germany. Germany will head to the polls for an early federal election after the coalition government led by Chancellor Olaf Scholz lost a no-confidence vote in December. This week Germany’s Christian Democrats, led by Friedric Merz, have introduced plans for tougher migration measures, with votes from the far-right Alternative for Germany (AfD) party supporting these plans.This move led Scholz to say that he could not work with the CD party. Polls suggest the AfD, led by Alice Weidel, could finish second with a record 20% of the vote on 23 February. The former coalition of the SPD, the Greens and the Free Democrats (FDP), has lost substantial support in the polls.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

Questo articolo viene fornito all'utente soltanto a scopo informativo e non deve essere considerato come un'offerta o una sollecitazione di un'offerta di acquisto o di vendita di investimenti o servizi correlati che possono essere qui menzionati.