Will the oil price surge pull economies off course?

Corporate Earnings Calendar

Thursday: JD Sports Fashion, CostCo Wholesale, Kroger, Burlington Stores

Tuesday: Franco Nevada, Toll Brothers

Wednesday: Uipath, Tourmaline Oil

Global Macro Updates

Middle East war spreads. On Wednesday the conflict in the Middle East escalated with the US downing of an Iranian submarine off the coast of Sri Lanka. General Dan Caine, Chair of the US joint chiefs of staff, said the attack was the first time since 1945 that a US submarine used a torpedo to sink an enemy combatant ship. It came as the US Senate, in a 47-53 vote, cleared the way for President Donald Trump to continue military attacks on Iran. The House will vote on its own resolution on Thursday; this is now a purely symbolic gesture since legislation to end the war would have to pass both chambers of Congress. On Wednesday there were also reports of US talks with Iranian Kurdish militants over anti-regime operations. White House press secretary Karoline Leavitt said that Donald Trump “did speak to Kurdish leaders with respect to our base that we have in northern Iraq”, but she added that the president had not agreed to “any such plan” to arm and equip Iranian Kurdish fighters. According to a Financial Times report, Iran’s intelligence ministry on Wednesday said it destroyed headquarters and munitions depots of Iranian Kurdish groups in Iraq, accusing them of “planning to infiltrate the country’s western borders” with US and Israeli support “to fulfil their separatist objectives in urban and border areas”. News of these talks came as Turkey said NATO air defences intercepted a ballistic missile launched from Iran. Turkey has a significant Kurdish population and has been battling a decades-long insurgency against the Kurdistan Workers’ Party (PKK) in Turkey and in Iraqi Kurdistan. The PKK is closely allied to one of the largest of the Iranian armed groups, the Kurdistan Free Life Party or PJAK.

Mixed economic signals from the US. Despite worries that the US-Israeli led war against Iran could damage the US economy, there are still signs that the US economy is growing and that employment may be stabilising. According to the Institute for Supply Management, its services index rose 2.3 points to 56.1, above expectations of 53.5 and January’s 53.8. It was the highest headline level since August 2022. The rise was due to robust orders growth and business activity while prices paid declined. Fourteen service industries reported growth in February, led by mining, information and real estate, while three contracted. However, the final S&P Global US services PMI for February came in at 51.7 vs 52.3 consensus. S&P said the slowdown was accompanied by only a moderate rise in incoming new business, with both activity and sales hindered somewhat by adverse weather conditions. Nonetheless, muted demand conditions limited hiring activity with employment growth largely associated with filling existing vacancies, and kept business confidence was below trend. In contrast, February ADP reported that private payrolls grew by 63K, better than the 50K consensus and higher than the prior month's 11K (revised down from 22K). This was the most jobs added since July. Hiring was concentrated in only a few sectors, with education and health services seeing the largest gains. As reported by Bloomberg news, the ADP report showed workers who changed jobs saw a 6.3% increase in pay from a year earlier, a slowdown from January. Wage growth for those who stayed put held at 4.5%. The Fed's Beige Book said economic activity increased at a slight to moderate pace in seven of 12 districts, though flat or declining in five others. The report noted that employment levels were generally stable, even as firms looked to artificial intelligence to bolster efficiency.

Although the US economy appears to still be relatively stable, consumers may soon feel the effects of continued tariffs on domestic prices as US Treasury secretary Scott Bessent has said that the global tariff the White House imposed following its Supreme Court defeat will probably be lifted from 105 to 15% this week. The previous tariff regime was struck down by the US Supreme Court on 20th February. The Trump administration invoked Section 122 of the Trade Act of 1974, to immediately impose fresh levies on imports to the US for 150 days.

Global market indices

US Stock Indices Price Performance

Nasdaq 100 +0.54% MTD and -0.62% YTD

Dow Jones Industrial Average -0.49% MTD and +1.41% YTD

NYSE -1.74% MTD and +4.92% YTD

S&P 500 -0.14% MTD and +0.35% YTD

The S&P 500 is -1.10% over the past seven days, with 7 of the 11 sectors down MTD. The Equally Weighted version of the S&P 500 is -0.32% over this past week and -1.04% YTD.

The S&P 500 Information Technology is the leading sector so far this month, +1.12% MTD and -4.55% YTD, while Materials is the weakest sector at -3.17% MTD and +13.91% YTD.

Over the past seven days, Energy outperformed within the S&P 500 at +2.20%, followed by Real Estate and Communication Services at +0.74% and +0.30%, respectively. Conversely, Information Technology underperformed at -2.87%, followed by Materials and Consumer Staples at -2.48% and -1.73%, respectively.

The equal-weight version of the S&P 500 was +0.40% on Wednesday, underperforming its cap-weighted counterpart by 0.38 percentage points.

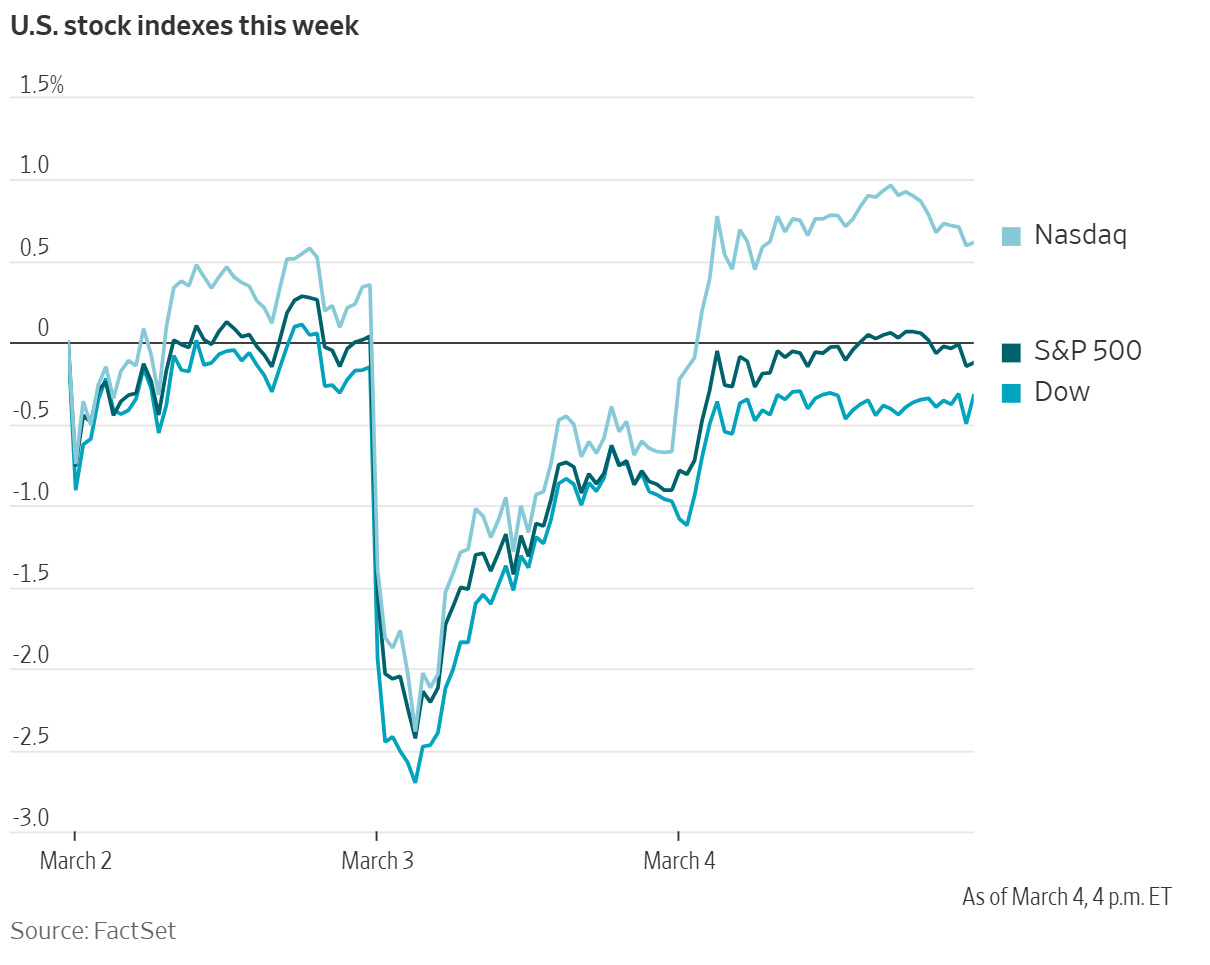

On Wednesday stocks advanced after a news report that Iran had signalled a willingness to talk and a pledge by President Donald Trump to steady oil markets. The Nasdaq Composite gained 290.79 points, or +1.29%, to 22,807.48. The Dow Jones Industrial Average rose, or +0.49%, to 48,738.98. The S&P 500 added 52.83 points, or +0.78%, to end at 6,869.46 points despite energy sector stocks falling, having climbed over the past few days on rising oil price fears. Over the past seven days, the S&P 500 is -1.10%, the Dow Jones -1.5%, and the Nasdaq Composite -1.49%.

In corporate news, Intel’s chief financial officer said server demand is still strong amid a supply shortage.

Investment banking giant Morgan Stanley laid off about 3% of its workforce, or roughly 2,500 employees, across all divisions on Wednesday. The job cuts were across the bank's three major divisions, investment banking and trading, wealth management and investment management.

Apple introduced the $599 MacBook Neo on Wednesday, signifying its biggest push yet into low-end laptops.

Alphabet’s Google unveiled a new system for apps on its Android phones and tablets.

In its fiscal Q1 2026 corporate earnings report released on Wednesday, chip designer Broadcom projected its artificial intelligence chip revenue would exceed $100 billion next year with CEO Hock Tan touting progress from Anthropic, Meta and OpenAI.

Mega caps: The Magnificent Seven had a mixed performance over the past week. Over the last seven days, Amazon +2.93%, Microsoft +1.15%, and Meta Platforms +2.15%, while Nvidia -6.40%, Tesla -2.75%, Alphabet -3.12%, and Apple -4.27%.

Energy stocks had a largely positive performance this week although energy service companies were down due to a combination of profit-taking, sector rotation, and lingering concerns over North American oilfield service activity. The Energy sector itself +2.20%. WTI and Brent prices are +14.28% and +15.15%, respectively, over the past week. Over the last seven days, APA +11.71%, Chevron +0.98%, Occidental Petroleum +5.25%, Shell +1.74%, BP +2.34%, Phillips 66 +8.43%, ExxonMobil +0.51%, Marathon Petroleum +12.77%, and ConocoPhillips +5.13%, while Baker Hughes -6.06%, Halliburton -2.38%, and Energy Fuels -3.72%.

Materials and Mining stocks had a very mixed performance this week, with the Materials sector itself -2.48%. Over the past seven days, Yara International +2.89%, Celanese Corporation +2.24%, CF Industries +8.91%, and Nucor +0.34%, while Albemarle -14,05%, Freeport-McMoRan -4.20%, Mosaic -3.60%, Sibanye Stillwater -8.27%, and Newmont Corporation -4.39%.

European Stock Indices Price Performance

Stoxx 600 -3.34% MTD and +3.47% YTD

DAX -4.27% MTD and -1.16% YTD

CAC 40 -4.81% MTD and +0.22% YTD

IBEX 35 -4.76% MTD and +1.04% YTD

FTSE MIB -5.81% MTD and -1.06% YTD

FTSE 100 -3.14% MTD and +6.41% YTD

This week, the pan-European Stoxx Europe 600 index is -3.28%. It was +1.37% Wednesday, closing at 612.71.

So far this month in the STOXX Europe 600, Oil & Gas is the leading sector +0.28% MTD and +18.98% YTD, while Personal & Household is the weakest at -5.97% MTD and -5.66% YTD.

Over the past seven days, Oil & Gas outperformed within the STOXX Europe 600, at +0.83%, followed by Financial Services and Telecom at +0.78% and -0.51%, respectively. Conversely, Banks underperformed at -6.55%, followed by Personal & Household and Basic Resources at -6.22% and -5.40%, respectively.

Germany's DAX index was +1.74% Wednesday, closing at 414.71. It was -3.86% over the past seven days. France's CAC 40 index was +0.79% Wednesday, closing at 8,167.73. It was -4.57% over the past week.

The UK's FTSE 100 index was -2.2% over the past seven days to 10,567.65. It was +0.80% on Wednesday.

In Wednesday's trading session,Travel & Leisure, Defence, Technology and Banks led; while Food& Beverage, Chemicals and Oil& Gas lagged. This followed a deep selloff in two previous sessions.

Other Global Stock Indices Price Performance

MSCI World Index -2.19% MTD and +0.60% YTD

Hang Seng -5.19% MTD and -1.49% YTD

Over the past seven days, the MSCI World Index and Hang Seng Index are -2.65% and -5.66%, respectively. The drop in Hang Seng may be a precursor of expected slower growth in the Chinese economy this year. On Wednesday China set its lowest growth target for GDP in decades, aiming for GDP growth between 4.5 and 5% in 2026. The government said it would maintain a higher fiscal deficit as leaders warned of growing “difficulties and challenges” in the economy. The lowering of the GDP forecasts suggests that the government may implement fewer expansionary fiscal policies this year as it targets its longer-term development goal of reaching “mid-level” developed-economy income by 2035 over short-term growth.

However, according to the Financial Times, China’s Premier Li Qiang said on Thursday that defence spending would rise 7 per cent this year, slightly lower than 7.2 per cent a year ago but still significantly outpacing overall fiscal expenditure as he warned against Taiwan's “independence”.

Currencies

EUR -1,57% MTD and -1.00% YTD to $1.1630

GBP -0.83% MTD and -0.74% YTD to $1.3373

The dollar index fell on Wednesday, -0.25% to 98.80. However, over the week, the dollar index was up +1.13%, reaching three-month highs as the fallout from the Middle East conflict prompted a flight to the safe-haven currency. The spike in energy prices from the conflict is stoking fears of a resurgence in inflation and worrying investors about the US rate outlook if energy supplies become constrained. The dollar index is +1.22% MTD and +0.49% YTD.

The euro was up +0.16% to $1.1630 on Wednesday. However, the euro was -1.53% over the last seven days as investors flocked to the US dollar as fears grew that rising energy price pressures will cause a rise in inflation and weigh on future ECB policy decisions. Sterling was +0.13% to $1.3373, but it was -1.38% over the last seven days.

Against the Japanese yen, the dollar fell -0.43% to ¥157.07 per dollar on Wednesday. The dollar was +0.45% against the Japanese yen over the past seven days. It is +0.65% MTD and +0.25% YTD.

Note: As of 5:00 pm EST 4 March 2026

Cryptocurrencies

Bitcoin +11.42% MTD and -16.17% YTD to $73,389.00

Ethereum +11.54% MTD and -27.52% YTD to $2,151.11

Bitcoin was +8.36% over the last seven days and Ethereum was +8.27% as the cryptocurrencies appeared more stable relative to other assets, including gold, which saw selloffs following US and Israeli strikes on Iran last weekend. On Wednesday, Bitcoin finally broke out of a month-long consolidation and rallied +7.25% to $73,289. Ethereum rose +8.27% to $2,152.11. So far in March, investors have poured more than $1.1 billion into US Spot Bitcoin ETFs, including $462 million on Wednesday, according to data compiled by Bloomberg. These flows are seen as a key barometer of confidence in the wider market. This uptick offered a glimmer of hope, but the overall macro outlook remains a concern given the rise in geopolitical tensions accompanying the widening of the conflict beyond the GCC region to Turkey, Lebanon, and Cyprus.

On a positive note, there are hopes that cryptocurrencies may benefit from increasing regulatory clarity in the US. The US Securities and Exchange Commission (SEC) has submitted an interpretive guidance to the White House outlining how securities laws could be applied to cryptocurrencies. As reported by The Block, the guidance, titled "Commission Interpretation on Application of the Federal Securities Laws to Certain Types of Crypto Assets and Certain Transactions Involving Crypto Assets," was submitted on 3 March and is currently at the prerule stage undergoing interagency review. SEC Chairman Paul Atkins has previously stated the regulator will consider interpretive guidance around a token taxonomy for crypto assets in line with market structure legislation. Accordingly, as noted by Bloomberg news, a token taxonomy could in theory establish formal categories for different types of crypto assets, determining, for instance, whether a given token is treated as a security subject to SEC oversight or under the CFTC’s jurisdiction.

Note: As of 5:00 pm EST 4 March 2026

Fixed Income

US 10-year yield +12.9 bps MTD and -7.9 bps YTD to 4.090%

German 10-year yield bps +9.3 MTD and -9.1 bps YTD to 2.767%

UK 10-year yield bps +14.7 bps MTD and -7.8 bps YTD to 4.395%

US Treasury yields rose for a third straight day on Wednesday as investors weighed the potential risk of rising inflation on monetary policy after the war in Iran elevated oil prices. Yields extended their gains after the Institute for Supply Management (ISM) said its nonmanufacturing purchasing managers index rose to 56.1 last month, the highest reading since July 2022, up from 53.8 in January.

The yield on the two-year Treasury note, sensitive to expectations for the Fed funds rate policy, was +4 bps to 3.543%. The 10-year US Treasury note yield was +3.2 bps to 4.090%. The yield on the 30-year Treasury bond was +2 bps to 4.723%.

The yield curve spread between two- and 10-year Treasury notes was at a positive 54.7 basis points on Wednesday. Over the past week, the yield curve spread between two-year and 10-year notes has dropped -3 bps.

Fed officials have stated that it will take time to assess the impact of the Iran conflict on monetary policy decisions, although Governor Stephen Miran said on Bloomberg TV on Wednesday that it had not changed the need for interest rate cuts. There are concerns that inflationary expectations could become unanchored if the conflict in the Middle East continues beyond a few weeks and the Strait of Hormuz remains closed to shipping as this would likely raise the price of oil and gas, with consequent inflationary effects.

Expectations for a rate cut by the Federal Reserve have fallen due to the rise in oil prices, with the June meeting now showing only a 35.5% chance for a cut of at least 25 basis points, according to CME Group's FedWatch Tool. Fed funds futures traders are now pricing in a 2.7% probability of a 25 bps rate cut at March’s FOMC meeting, down from 3.6% last week.

Across the Atlantic, in the UK, on Wednesday the 10-year gilt was -6.7 bps to 4.395%. Over the past seven days, it was +7.7 bps.

German government bond yields fell, with the two-year yield, highly responsive to interest rate expectations, -4.1 bps to 2.149%. The 10-year yield fell -4 bps to 2.767% after hitting 2.815% on Tuesday, its highest since 11 February. The 30-year yield was +3 bps to 3.412%.

Italy’s BTP 10-year yield was +1.4 bps on Wednesday to 3.453%. French OAT 10-year yield was +2 bps to 3.384%.

Over the past seven days, the German 10-year yield is +5.6 bps. Germany's two-year bond yield is +10.5 bps, while Germany's 30-year yield is +3 bps.

The yield spread between German Bunds and 10-year UK gilts reached 162.8 bps on Wednesday, a rise of +5.4 bps over the past seven days.

The spread between US 10-year Treasuries and German Bunds is now 132.3 bps, +3.6 bps from last week’s 128.7 bps.

The spread between Italian BTP 10-year yields and German Bund 10-year yields fell 7 bps to stand at 67 after widening 10 bps on Tuesday. The Italian 10-year yield was +14.7 bps over the last week.

Over the course of the week, France’s 10-year yield has risen +12.6 bps. The spread between the French OAT 10-year yield and German Bund 10-year yield stood at 61.7 bps, 5 bps more than last week’s 54.7 bps.

Money markets increased bets ECB rate hikes, but continued to price in less than a 50% chance of such a move by year‑end. They indicated around a 30% chance of tightening by December, down from over 60% on Tuesday. They also indicated a 35% chance of a hike by June 2027.

This comes as the widening conflict in the Middle East disrupts LNG production and shipments, tightening supply and sending prices soaring. Stocks are set to end the heating season far below normal levels, forcing Europe to buy more gas during the summer when it refills its storage facilities, which in turn underpin the region’s energy security. Energy price inflation will likely weigh on future ECB decisions, but ECB policymakers such as Bank of France Governor François Villeroy de Galhau are saying there is no reason for the ECB to raise its interests rates, despite the on-going conflict in the Middle-East, and that financial stability is currently not at risk, but much will depend on how long the conflict lasts.

Commodities

Gold spot -2.11% MTD and +18.37% YTD to $5,120.20 per ounce

Silver spot -10.22% MTD and +18.64% YTD to $83.76 per ounce

West Texas Intermediate crude +11.38% MTD and +30.25% YTD to $74.66 a barrel

Brent crude +11.71% MTD and +33.77% YTD to $74.66 a barrel

Gold rose on Wednesday, as the escalating conflict in the Middle East attracted safe‑haven investors and a slight fall in the dollar also lent support. Spot gold was +0.25%, reaching $5,120.20 per ounce. Over the last seven days, spot gold prices have fallen -1.66%. Spot gold was -2.11% MTD but still +18.37% YTD.

Spot silver was +0.34% to $83.76 per ounce. Over the last week, spot silver prices have fallen -7.94%. Spot silver is -10.22% MTD, but still +18.64% YTD.

Oil prices whipsawed on Wednesday as investors assessed the widening impact of the US-Iran war on Middle East energy markets. The war in the Middle East widened after a US strike hit an Iranian warship off Sri Lanka and NATO air defences destroyed an Iranian ballistic missile that had been fired towards Turkey. There was no shipping through the Strait of Hormuz for a fifth day, choking off vital Middle East oil and gas flows to Europe and Asia.

Brent crude settled at $82.60 per barrel, +1.47%, staying at its highest since January 2025. US WTI crude settled 10 cents, or +0.13%, at $74.66, closing at its highest since June for the second day in a row. It surged roughly 11% in the previous two sessions.

Over the last seven days, WTI is +14.28% and Brent is +15.15%.

EIA report. The latest US Energy Information Agency (EIA) report released on Wednesday showed that US crude stocks rose to their highest level in three and a half years last week as exports and imports declined. Crude inventories rose by 3.5 million barrels to 439.3 million barrels in the week ended 27 February. This was 180 thousand barrels per day more than the previous week’s.

Crude stocks at the Cushing, Oklahoma, delivery hub rose by 1.6 million barrels in the week, hitting their highest level since August 2024.

According to the EIA, average US crude oil imports averaged 6.3 million barrels per day last week, down by 335 thousand barrels per day from the previous week. Over the past four weeks, crude oil imports averaged about 6.6 million barrels per day, 10.3% more than the same four-week period last year. Net US crude imports fell last week by 19,000 barrels per day, EIA said, while exports declined by 316,000 bpd to roughly 4 million bpd. US commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) increased by 3.5 million barrels from the previous week. At 439.3 million barrels, US crude oil inventories are about 3% below the five year average for this time of year.

Refinery crude runs rose by 180,000 barrels per day, while utilisation rates edged up by 0.6 percentage points in the week to 89.2%. Total product supplied, a proxy for demand, fell by 1.59 million bpd to 19.87 million bpd.

Distillate stockpiles including diesel and heating oil, were up by 429,000 barrels in the week to 120.8 million barrels, versus expectations for a 2.6 million-barrel drop. US gasoline stocks fell by 1.7 million barrels.

Note: As of 5:00 pm EST 4 March 2026

Key data to move markets

EUROPE

Thursday: Eurozone Retail Sales, ECB Monetary Policy Meeting Accounts, and speeches by ECB Vice President Luis de Guindos, Austrian central bank Governor Martin Kocher, and ECB President Christine Lagarde

Friday: German Factory Orders, Eurozone Employment Change, Eurozone GDP, speeches by ECB President Christine Lagarde and ECB Executive Board Members Piero Cipollone and Isabel Schnabel

Monday: German Industrial Production and Eurozone Sentix Investor Confidence

Tuesday: German Trade Balance

Wednesday: German Harmonised Index of Consumer Prices

UK

Tuesday: BRC Like-for-Like Retail Sales

Wednesday: BoE Monetary Policy Report Hearings

USA

Thursday: Initial and Continuing Jobless Claims, Nonfarm Productivity, Unit Labour Costs, and a speech by Federal Reserve Vice Chair for Supervision Michelle Bowman

Friday: Nonfarm Payrolls, Average Hourly Earnings, Labour Force Participation Rate, Unemployment Rate, U6 Underemployment Rate, Retail Sales, Fed Monetary Policy Report and speeches by San Francisco Fed President Mary Daly, Philadelphia Fed President Anna Paulson, Cleveland Fed President Beth Hammack and Boston Fed President Susan Collins

Sunday: US Daylight Savings Time (clocks go forward one hour)

Tuesday: ADP Employment Change 4-Week Average and Existing Home Sales Change

JAPAN

Sunday: Current Account and Labour Cash Earnings

Monday: GDP

CHINA

Sunday: CPI and PPI

Tuesday: Exports, Imports and Trade Balance

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

本文提供给您仅供信息参考之用,不应被视为认购或销售此处提及任何投资或相关服务的优惠招揽或游说。金融工具交易存在重大亏损风险,未必适合所有投资者。过往表现并非未来业绩的可靠指标。

由专业人士创建。 为专业人士。