Fixed Income Briefing June 2026

Renée Friedman, Global Head of Research

Economic and US Treasury Market Review

• The dollar has risen by +2.66% MTD in June as the Fed has taken on a more hawkish tone under the leadership of its new chair, Kevin Warsh. During his first meeting as chair on 18 June, the Fed held rates at the 3.50 - 3.75% range, but he set a hawkish tone that reshaped near-term rate expectations. The dot plot forecast marked a decisive inflection: nine officials now project at least one rate hike in 2026, up from none in March, while markets now assign close to a 90% probability of a hike by year-end. There are no cuts projected in 2026 and the easing bias was removed from the policy statement. Warsh declined to produce his own dot plot and announced five task forces to examine the Fed’s communications, balance sheet, data sources, productivity and inflation frameworks,

• On the growth front, US economic data released in June indicates that the US economy is faring very well. The US Bureau for Labor Statistics showed that the US labour market in May 2026 added 172,000 non-farm payroll jobs and the national unemployment rate was unchanged at 4.3%. Average hourly earnings rose by 0.3%, but are up by 3.4% y/o/y.

• On the growth front, business activity rose again in June, with the S&P Global Flash US Composite PMI coming in at 52.2, up from May’s 51.5 and a 5-month high. The Flash Services PMI came in at 51.3, up from May’s 50.7, and a 4-month high. The Flash Manufacturing PMI reached a 49-month high, coming in at 55.7 from May’s 55.1. However, the growth was at least partly attributable to demand being temporarily supported by the front-running of potential supply issues and price hikes associated with the war with Iran. Supply chain delays grew more widespread in June. Supplier delivery times lengthened on average to the greatest extent since August 2022 and employment fell for a second month running in June as companies continued to focus on cost reduction amid high input prices and concerns over the outlook.

• On the consumer side, the preliminary June reading of the University of Michigan Confidence survey rose to 48.9, up from May's record low of 44.8 as lower gasoline prices provided some relief, particularly to lower income consumers. Sentiment is currently 13% below January 2026 and 19% below a year ago, as consumers continue to feel the rise in inflation. Year-ahead inflation expectations edged down from 4.8% in May to 4.6% this month. However, this still exceeds the 3.4% reading seen in February 2026 prior to the start of the Iran conflict. Long-run inflation expectations fell from 3.9% last month to 3.4% in June. CPI rose in line with expectations in May. Annualised inflation rose to 4.2% in May according to the Bureau for Labor Statistics. This is the highest rate in three years. It rose 0.5% m/o/m. Core inflation rose slightly below the estimate of 0.3%, instead coming in at 0.2% m/o/m while annualised core inflation came in at 2.9%, in line with expectations.

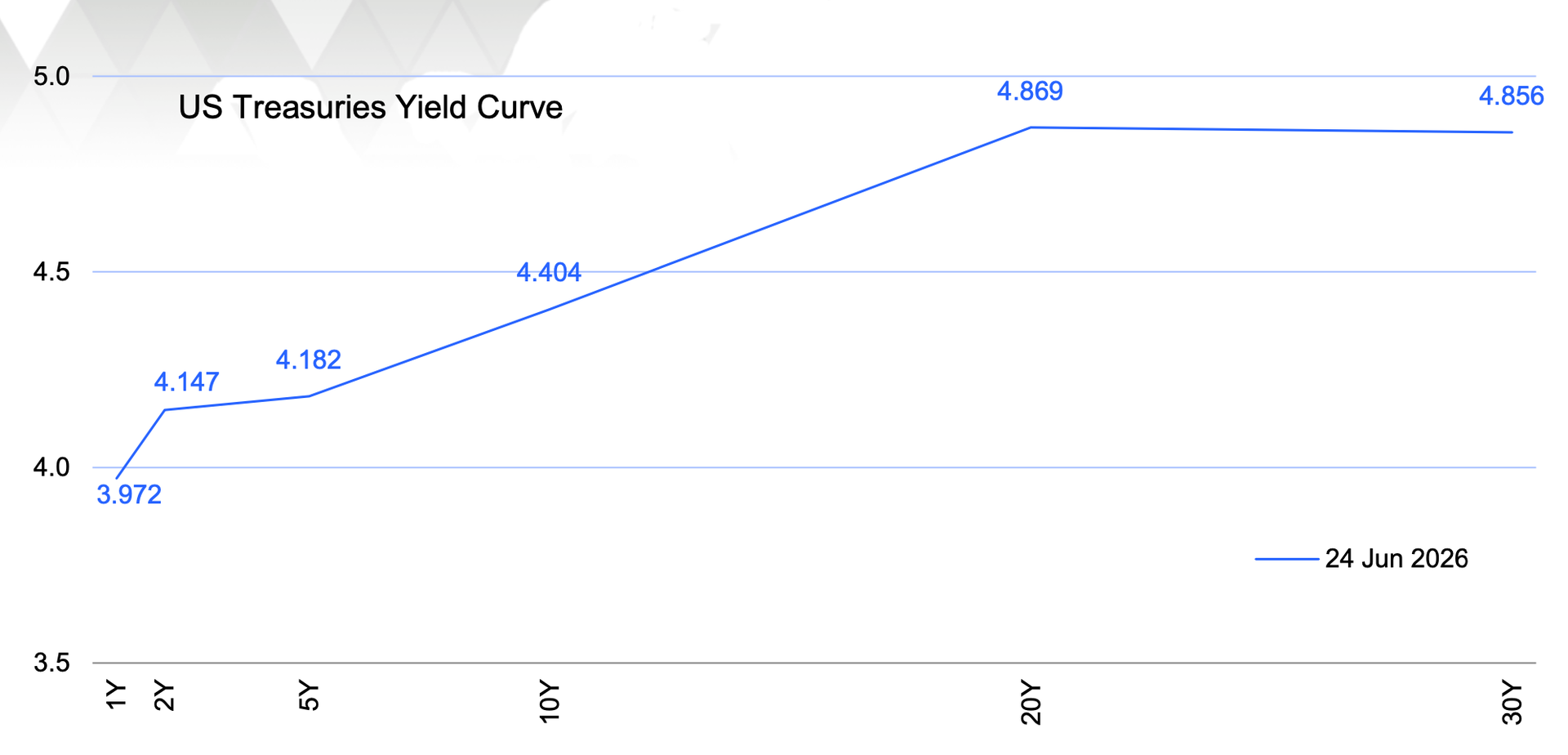

Yield swings

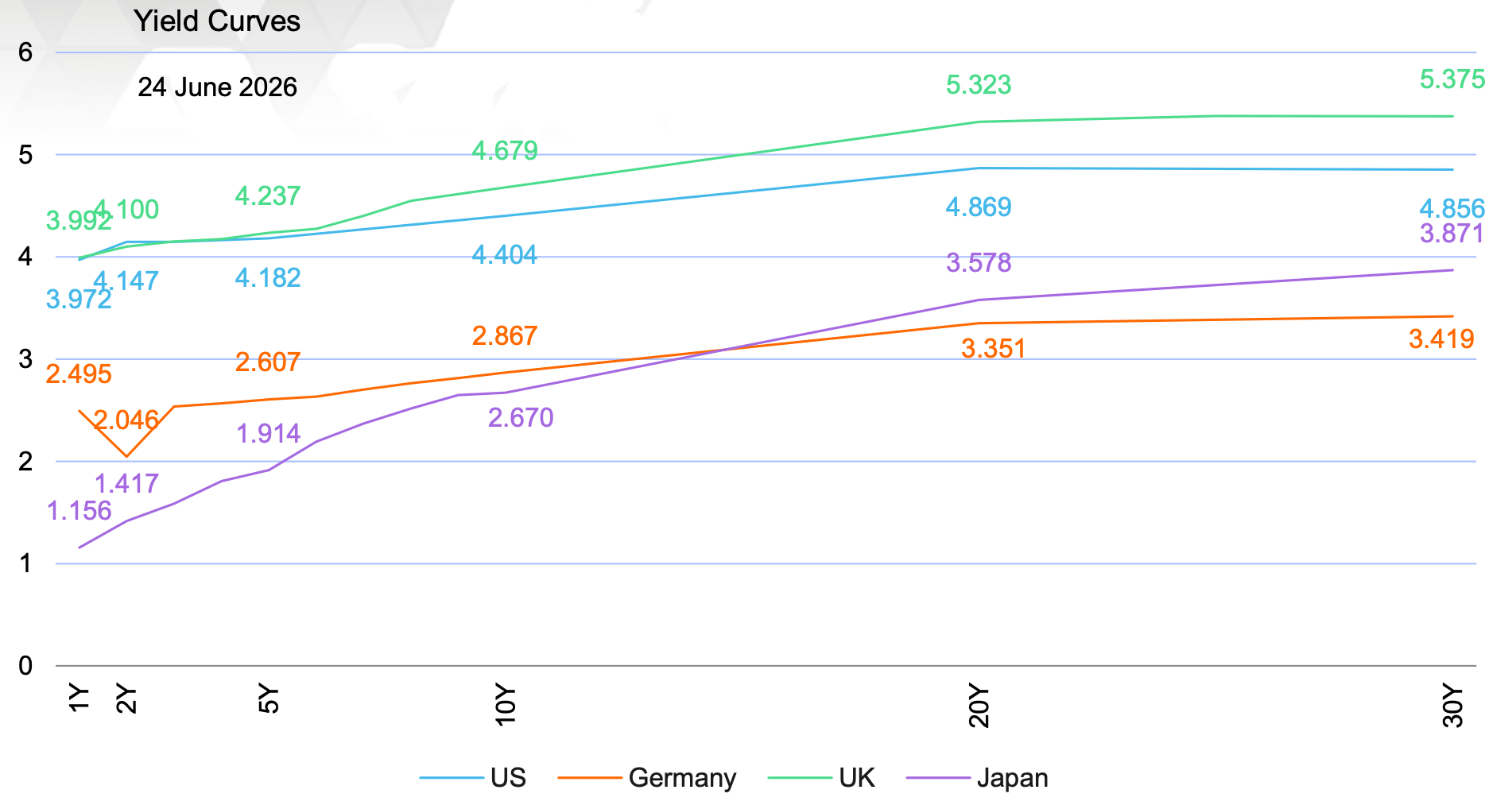

June has been another volatile month for bonds as investors reacted to signs that the US-led war with Iran may be ending, with oil prices plunging back to pre-Iran war levels and inflation expectations falling. The US yield curve has bear flattened with yields falling at the longer end. In the UK, domestic political uncertainty caused gilt yields to rise, but expectations of a relatively smooth political transition following Prime Minister Sir Keir Starmer's resignation and weaker UK flash PMI data has reinforced expectations of slower economic momentum. The ECB’s 25 bps hike in June led to increased volatility across German Bunds and kept borrowing costs elevated. However, yields have fallen following comments from ECB President Christine Lagarde, who told the European Parliament that there was no evidence of an inflation pickup that would justify more forceful policy action. The shift in sentiment was reinforced by the 60-day ceasefire between the US and Iran, which allowed shipping to resume through the Strait of Hormuz. The resulting drop in Brent crude prices reduced concerns that energy costs would feed into broader inflation pressures. Markets are still pricing in one additional 25 bps increase by the ECB by year-end, following its policy tightening earlier this month. However, investors now see little likelihood of a third move in 2026.

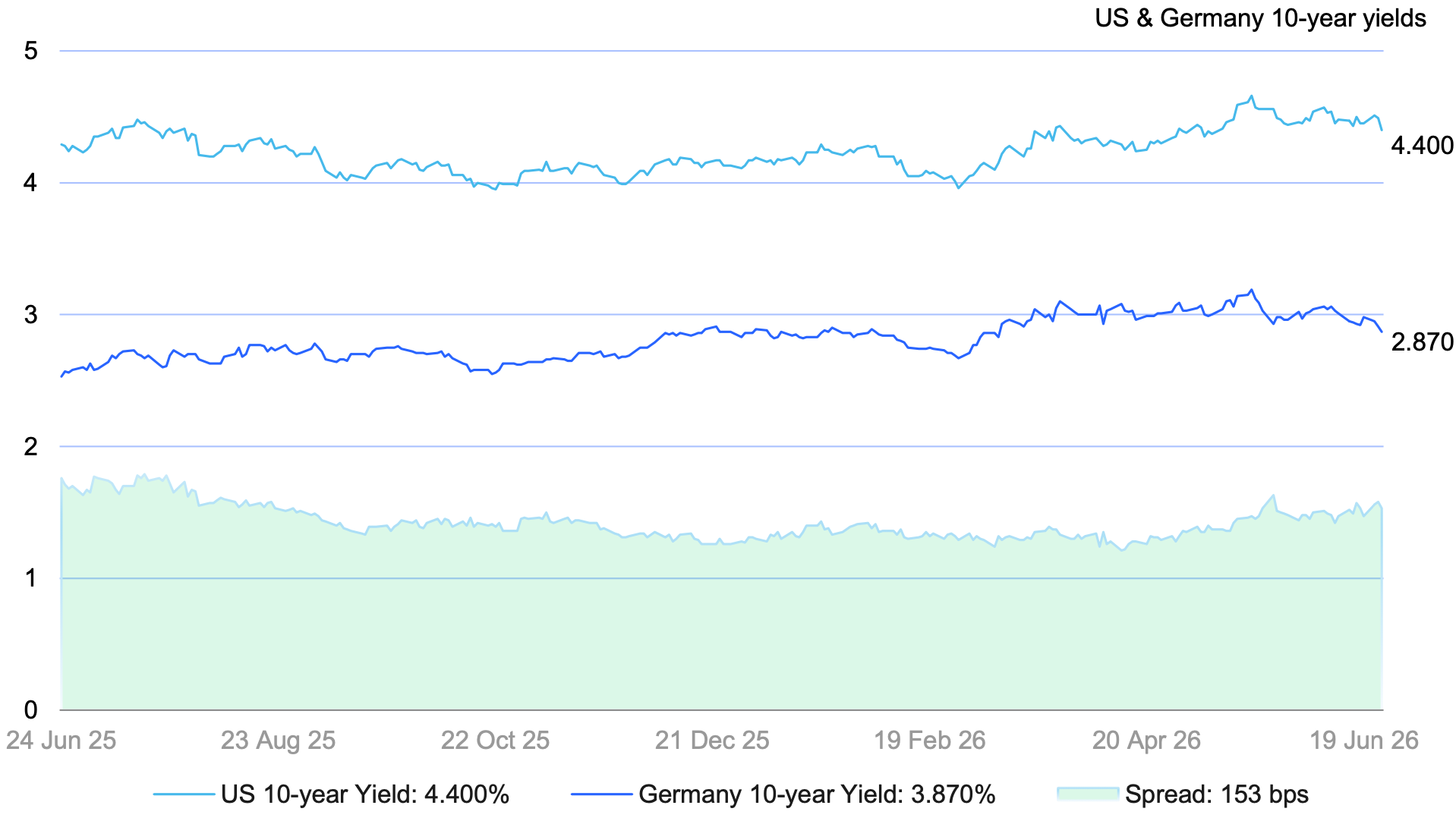

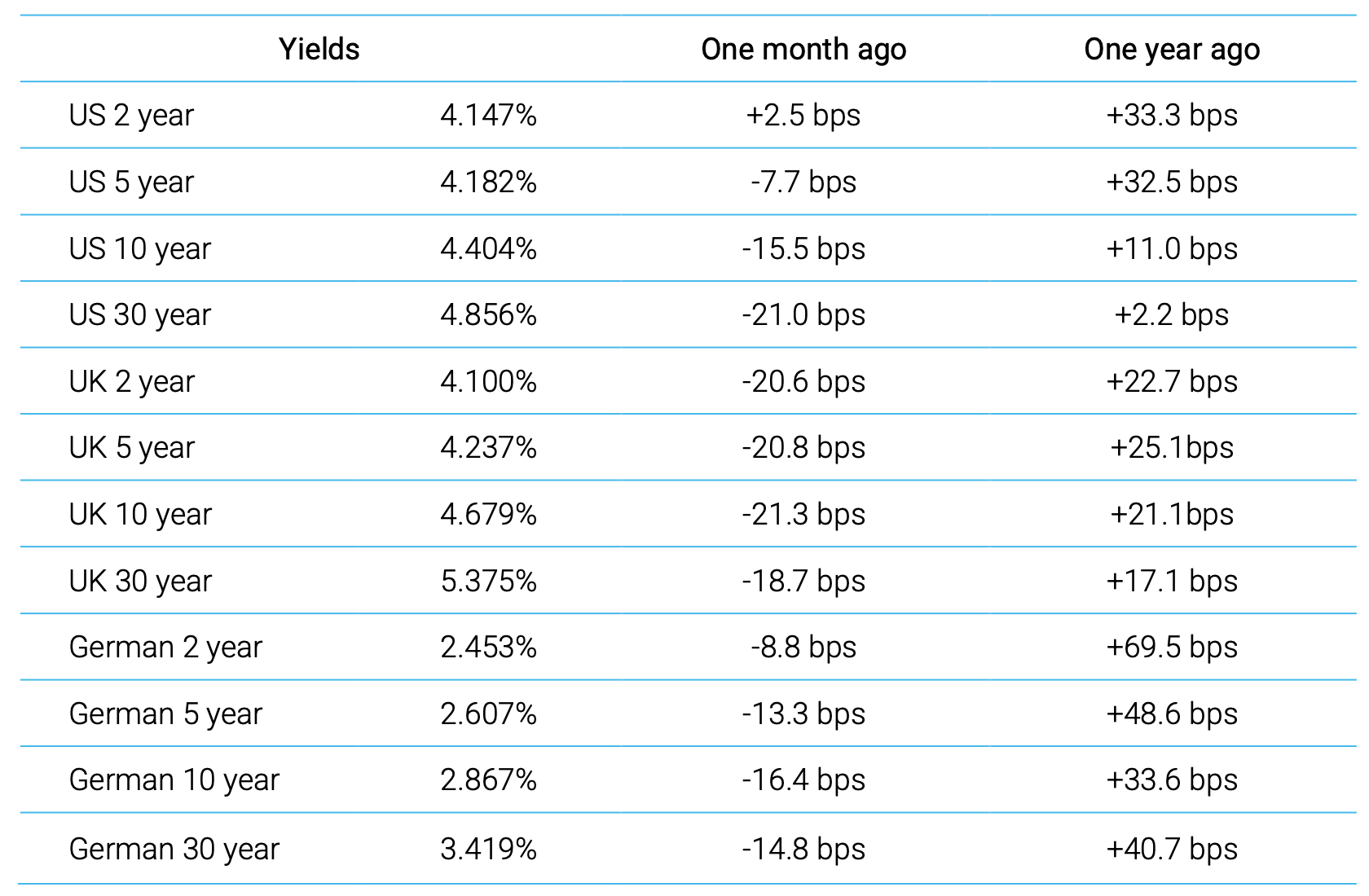

The US 10-year yield is -15.5 basis points (bps) from a month ago. The 10-year German Bund is -16.4 bps. The spread between the two has risen from 150.1 bps from the end of May to 152.5 bps. On the long-end of the curve, the US 30-year yield is -21 bps from a month ago, while the German 30-year yield is -14.8 bps from a month ago.

Source: FactSet

Source: FactSet

Source: FactSet 5:00 PM EST 24 June 2026

Global Economic and Market Review

The eurozone is showing some signs of resilience after a year of weakness. Eurozone headline inflation rose to 3.2% in May 2026, up from 3.0% in April. The S&P Eurozone Flash Composite PMI for June, rising to 49.5 from 48.5 in May. Although the index remained below the 50 threshold for a third consecutive month, the reading marked a 3-month high and signalled a clear moderation in the pace of decline. The Flash Services PMI was also at a 3-month high, coming in at 48.9, up from May’s 47.7. The Flash Manufacturing PMI slipped to 51.3, down from May’s 51.6 and a 4-month low. Overall, price pressures continued to moderate, as input-cost inflation fell to its weakest level since February and output-price growth eased to a three-month low. Supply-chain strains persisted, but became less severe. Employment recorded its smallest decline since February. Business confidence also improved for a second consecutive month, although it remained subdued by historical standards. Germany, Europe’s largest economy, continued to see its growth decline, with its composite PMI falling to an 18-month low amid weaker services activity.

European consumers are also becoming more confident. According to the European Commission, the flash estimate of the consumer confidence indicator showed an improvement in the EU, +1.2 percentage points compared with May, to -17.7. However, consumer confidence remains well below its long-term average. The ECB’s wage tracker indicates negotiated wage growth with smoothed one-off payments of negotiated wage growth of 3.0% in 2025 and 2.6% in 2026. The headline ECB wage tracker averaged 1.8% in the first quarter, 2.1% in the second quarter and 2.6% in the third and fourth quarters. Although above the ECB’s target rate, wage growth rate of around 3% is considered balanced by the ECB.

In the UK, weaker service activity led to a drop in business activity in June. The S&P Global Flash Composite PMI fell to a 14-month low of 49.4, below the 50.5 consensus estimate and the prior reading of 49.7. Services activity declined to a 41-month low of 48.7 from May’s 49.3 reading. Manufacturing was more resilient at 53, but was below May’s 53.9 reading and a three-month low. This was the second consecutive month in which activity contracted, with new business volumes declining at the fastest pace in 14 months and contributing to a sharper fall in backlogs of work. The downturn in services was attributed to domestic political uncertainty and the impact of the Middle East conflict. In manufacturing, expansion continued to rely partly on anecdotal reports of strategic stockpiling, which may fade after providing temporary support. Headline inflation in the UK remained steady in May, matching April’s 2.8% annualised rate. This was largely attributed to lower food costs offsetting price pressures from air fares, vehicle taxes and petrol. However, price growth in the services sector climbed to 3.7%. However, core inflation was up in May, rising 2.6% annualised, up from 2.5% in April; the CPI goods annual rate slowed from 2.4% to 2.0%, while the CPI services annual rate rose from 3.2% to 3.7%. According to the Office for National Statistics (ONS) June 2026 release, the unemployment rate is 4.9%. The economic inactivity rate rose by 0.1 percentage points to 21%. The early estimate of payrolled employees for May 2026 decreased by 119,000 (0.4%) on the year, but was largely unchanged on the month, increasing by just 2,000 (0.0%) to 30.3 million. The labour market is becoming increasingly fragile with job vacancies falling 19,000 over the quarter and down 31,000 on an annual basis.

Things to think about

Markets have reacted positively to the 60-day agreed ceasefire with Iran despite conflicting reports from Iran and the US as to the terms of the Memorandum of Understanding (MOU) and the temporary relief for Iranian oil from US oil sanctions. The market is still pricing in interest rates rises as investors consider ongoing and future geopolitical disruptions, the risk of higher inflation from a strong US economy as payroll growth reaccelerates, AI investment inflates core CPI and there is more hawkish tone from global central banks. The competition for capital will remain strong as governments in the US, UK, Europe and Japan will continue to issue debt to finance persistent deficits, putting additional upward pressure on the longer end as will the growing issuance from corporate bonds related to AI investment. In the US, new Fed Chair Kevin Warsh and other FOMC members have signalled that the Fed is going to take a serious stand against persistent inflationary pressures, but the drop in guidance may lead to increasing volatility in bond markets.

With inflation still expected to rise as it will take time for the energy sector to recover in the GCC region if the war with Iran ends, there will also still be secondary effects manifesting. Credit is expected to remain tighter for longer although the growth slowdown in Europe and the UK means the ECB and the BoE may have to take on a more dovish tone than the Fed or BoJ. The BoE will remain data-dependent, with the MPC reluctant to raise rates quickly as it will likely pause to see if inflation continues to rise or if the slack in the labour market will be enough to hold off on a rate rise. It will have to balance economic contraction risks against inflation concerns at a time when the government is changing leadership. The fiscal policies of Sir Keir Starmer’s expected successor as Prime Minister, Andy Burnham, remain speculative. However, based on his prior comments, it is being reported that his government would seek to raise a variety of taxes, despite the negative impact that it may have on growth, and that it may ignore the current government’s fiscal rules and issue more debt.

Risk premiums should be expected to widen further as policy divergence emerges. Geopolitical uncertainty is still high; there is still a chance that there could be an escalation in the war with Iran and/or that it could be drawn out further than currently anticipated, causing the market to price a more aggressive Fed next year. Investors may wish to consider selective yield-spread targeting and continuing to diversify across geographies to reduce country-specific risks. With central banks generally adopting a more hawkish tone and refraining from aggressive rate cuts, the front-end of the yield curve appears to offer a strong risk-reward balance, particularly in Europe. Additionally, they may wish to use inflation-protected securities (e.g., TIPS) to hedge inflation risk.

Key risks

• Inflation risks continue to rise, further undermining consumer and business confidence. The full second order impacts from the war with Iran may not be fully felt. Tariffs also remain unresolved, with the Trump administration having to respond to the USMCA agreement by 1 July (to extend it 6 years or review again next year) and the temporary 10% global tariff implemented under Section 122 scheduled to expire on 24 July. The Trump administration is actively preparing to replace these bridging tariffs with broader, legally durable Section 301 tariffs. These could also feed through to inflation. Persistently high inflation could force more aggressive rate hikes; conversely, a sudden disinflation may lead to policy easing.

• Policy uncertainty. The central banks may get the timing of rate hikes wrong or we may see a faster divergence in policy than currently considered. Fiscal stimulus changes and political pressures, especially in the UK under the new government, may create further volatility. Uncertainty over policies to deal with the “K-shaped” economy may result in uneven economic outcomes and may lead to credit risks in certain sectors or regions of the US.

• Geopolitical tensions, re-alignments and events. Conflicts or re-alignments in Europe and/or Asia over trade or other policy measures can quickly shift safe-haven demand and risk premiums. Although the European parliament has adopted legislation to remove import duties on many US goods, fulfilling the EU's side of a trade deal struck with President Trump last year, thus avoiding a renewed transatlantic trade conflict, the situation around Chinese trade remains unresolved. Globally there is still the chance of US trade policy shifts under the Trump administration. In addition, it is not clear that the 60-day deal with Iran will hold given the variations in statements from the Iran vs the US side. These factors may drive significant supply chain disruptions and increase energy price volatility. Additionally geopolitical concerns such the threat to Taiwan from mainland China, the increase in military exercises by the Chinese navy in the South China Seas, the continued expansion of US military and political activities in Latin America, and the ongoing war in Ukraine, have all increased risk aversion, supporting demand for Treasuries as a safe haven.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.