Trading the ceasefire, mispricing the supply shock?

What to look out for today

Companies reporting on Monday, 20 April: Steel Dynamics

Key data to move markets today

EU: German PPI

Global Macro Updates

Risk premia denial. US equities are hitting record highs even as headlines point to rising stagflation risk and fatter risk premia ahead. This is creating a widening disconnect between current price action and the forward macro‑earnings picture.

Iran’s renewed closure of the Strait of Hormuz, including reports of gunfire on commercial vessels and a de facto halt in tanker traffic, threatens roughly a fifth of global oil flows and is disrupting shipping. The US’ expanded naval campaign, preparing to board Iran‑linked tankers on the high seas and deploying sea drones to clear mines, underscores that the energy supply is now hostage to potential open‑ended military and maritime confrontation. At the macro level, seven weeks of war are beginning to show up in survey data, with the IMF warning that higher energy prices are reviving stagflation risks, even if a ceasefire holds.

Equity bulls are leaning heavily on hopes of a US‑brokered peace and solid Q1 prints, but the forward‑looking indicators are flashing yellow. Trump has oscillated between threatening strikes on Iran’s power plants and bridges if no deal is reached. He also insisted a peace agreement will happen ‘one way or another and is dispatching Vice President Vance back to Pakistan for another round of talks.

On the ground, Iranian officials stress that maximalist US demands remain unacceptable and explicitly rule out shipping enriched uranium to the US, highlighting the distance to any durable settlement. At the same time, analysts are cutting US profit estimates, guidance momentum is the weakest since 2025, and the share of companies raising both earnings and revenue outlooks continues to fall, as reported by Bloomberg news, just as an energy‑driven inflation impulse threatens margins and valuations. The paradox is that markets are pricing a near‑perfect soft‑landing and quick peace dividend at precisely the moment when war‑related supply shocks and deteriorating corporate guidance argue for higher risk premia, not record‑low ones.

BoJ Governor Ueda's latest dovish comments. Remarks from BoJ Governor Kazuo Ueda, following the Washington G20 meeting, conveyed a dovish tone in both the yen and JGB markets. As reported by Nikkei, Ueda indicated that the Monetary Policy Committee ‘will take appropriate measures’ in response to ‘persistent shocks from the deterioration in the Middle East situation’.

During a joint press conference with Finance Minister Katayama after the central bank and finance ministers meeting, Ueda emphasised a strong consensus regarding the high level of uncertainty in the current environment. He noted the ongoing assessment of how rising crude oil prices may impact inflation and economic growth, stating that it remains challenging to determine an appropriate policy response. Ueda also stressed that Japan's circumstances differ from those of other nations, given its extremely low real interest rates and highly accommodative financial conditions.

Following the earlier G7 meeting, Minister Katayama observed that US and European members estimated it would take two to three weeks to evaluate the implications of developments in the Middle East. Reuters reported that the absence of explicit signals regarding an imminent policy move has increased speculation that an April rate hike is unlikely. Markets had priced in roughly a 70% probability of an April hike following more hawkish communications from the BoJ. However, after Governor Ueda's 13 April speech, which highlighted risks associated with the Middle East conflict, market expectations for an April hike dropped to 30%. His latest comments have since resulted in further declines in market pricing for an April hike, now estimated at around 10%.

US Stock Indices

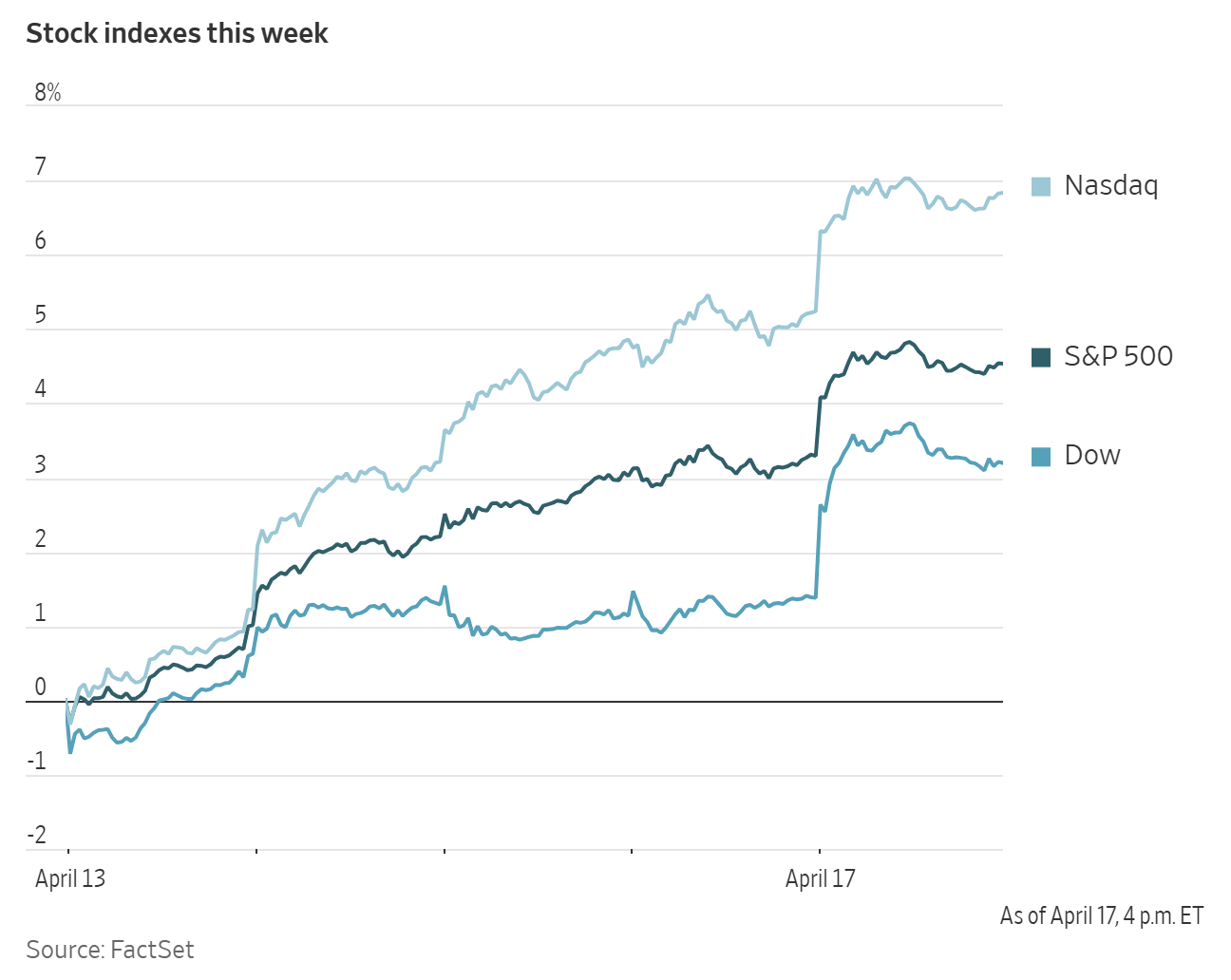

Dow Jones Industrial Average +1.79%

Nasdaq 100 +1.29%

S&P 500 +1.20%, with 9 of the 11 sectors of the S&P 500 up

There was a robust rally in equities on Friday, securing a third consecutive week of gains for major stock indices, on signs of progress toward resolving the Iran - US conflict.

The Dow Jones Industrial Average rose +1.79%, or 868.71 points. The S&P 500 and Nasdaq Composite also posted gains of +1.20% and +1.52%, respectively, each setting a new record high for the third consecutive session. Over the past three weeks, the S&P 500 and the Nasdaq Composite have registered their strongest performance since 2020.

The Nasdaq recorded a +6.84% gain for the week, marking its 13th consecutive session of advances, the longest such streak since 1992. The S&P 500 climbed +4.54% over the week, driven by strength in the Information Technology sector, which also extended its winning run to 13 days. Meanwhile, the Dow posted a weekly increase of +3.19%.

In corporate news, QVC commenced a voluntary Chapter 11 bankruptcy as part of a restructuring agreement with creditors.

A consortium including Bouygues Telecom, Orange and Iliad Group bid €20.4 billion for Altice Group’s French telecommunications operations. The deal would mark a significant consolidation of the French telecom market, reducing the number of players to three from four, and would relieve Altice's heavy debt burden.

Netflix shares dropped Friday after it reported disappointing guidance and said Chairman and co-founder Reed Hastings will step down from the board after his term expires in June.

S&P 500 Best performing sector

Consumer Discretionary +1.97%, with Royal Caribbean +7.34%, Carnival +6.99% and Mohawk Industries +6.54%

S&P 500 Worst performing sector

Energy -2.94%, with Valero Energy -7.48%, APA -5.70% and Marathon Petroleum -5.55%

Mega Caps

Alphabet +1.99%, Amazon +0.34%, Apple +2.59%, Meta Platforms +1.73%, Microsoft +0.60%, Nvidia +1.68% and Tesla +3.01%

Information Technology

Best performer: Analog Devices +4.99%

Worst performer: Oracle -1.84%

Materials and Mining

Best performer: International Flavors & Fragrances +5.30%

Worst performer: LyondellBasel Industries -11.98%

Corporate Earnings Reports

Posted on Friday, 17 April

Fifth Third Bancorp quarterly revenue +33.9% to $2.860 bn vs $2.845 bn estimate

EPS at $0.15 vs Loss Per Share $0.10 estimate

Tim Spence, President and CEO, said, “The first quarter reflected continued momentum across Fifth Third. We delivered strong loan and deposit growth, driven by new commercial relationships and continued household expansion. We closed the acquisition of Comerica on February 1st, and early financial benefits are already showing up, including strong net interest margin expansion and tangible book value per share growth. Integration is progressing as we expected. We have integrated the combined management teams and are retaining key customer-facing colleagues, supporting continuity for clients as we move forward as one organization. We are also seeing early revenue synergies across both commercial and consumer businesses.” — see report.

State Street quarterly revenue +15.6% to $3.796 bn vs $3.666 bn estimate

EPS at $2.49 vs $2.60 estimate

Ron O’Hanley, Chairman and CEO, said, “Our focus on being an essential partner to clients, supported by operational excellence and a diversified business model, enabled us to deliver a strong start to 2026 with growth underpinned by continued financial and strategic progress in the first quarter. Reflecting that progress, we delivered record quarterly fee revenue, net interest income, and total revenue, generating meaningful year-over-year positive operating leverage and pretax margin expansion, excluding notable items. In a dynamic operating environment, the momentum across Investment Services, Investment Management, and Markets underscores the strength of our franchise.” — see report.

European Stock Indices

CAC 40 +1.97%

DAX +2.27%

FTSE 100 +0.73%

Commodities

Gold spot +0.85% to $4,828.30 an ounce

Silver spot +3.04% to $80.79 an ounce

West Texas Intermediate -8.18% to $85.57 a barrel

Brent crude -6.14% to $91.99 a barrel

On Friday, gold prices continued to advance, bolstered by a weaker US dollar and diminishing inflationary pressures.

Spot gold increased +0.85% to $4,828.30 per ounce and was +1.70% over the week.

Indian banks have suspended gold and silver orders from international suppliers, with several tonnes held at customs due to the absence of a formal government authorisation for imports, according to trade sources.

Spot silver rose +3.04% to $80.79 per ounce and recorded a +6.47% increase for the week.

Oil prices plunged on Friday with both Brent and US WTI recording their largest daily losses since 8 April. This followed statements from Iran confirming that all commercial vessels would be permitted to pass through the Strait of Hormuz during the ongoing ceasefire and assurances from the US President that Iran had committed to keeping the strait open indefinitely.

Brent crude futures settled at $91.99 per barrel, reflecting a decrease of $6.02 or -6.14%, after reaching a session low of $86.09. US WTI crude futures closed at $85.57 per barrel, dropping $7.62 or -8.18%, after dipping to a low of $80.56.

Over the previous week, WTI fell -10.52%, while Brent crude declined -2.59%.

According to a senior Iranian official quoted by Reuters, all vessels may traverse the Strait of Hormuz provided coordination with Iran’s Islamic Revolutionary Guard Corps. The unfreezing of Iranian assets was reportedly a component of the agreement.

As the market swiftly unwound the heightened risk premium accumulated over the past few weeks, crude prices began to reflect normalised flows rather than disruption concerns. Ship tracking data indicated that approximately 20 vessels were moving out of the Gulf via the Strait of Hormuz.

A three-page memorandum of understanding to resolve the conflict has been developed, according to Axios.

During a phone interview with Reuters, President Trump stated that the US would retrieve its enriched uranium from Iran at a ‘leisurely pace.’

Oil prices had already declined early in Friday’s trading session amid prospects for additional negotiations between the US and Iran over the weekend and the implementation of a 10-day ceasefire between Lebanon and Israel, fostering optimism that the Middle East conflict might be approaching resolution.

Addressing a key issue in the negotiations, the US President noted that Tehran had offered to refrain from possessing nuclear weapons for more than 20 years. The US President also announced that the US has prohibited Israel from conducting further airstrikes in Lebanon, employing a notably firmer stance with its ally.

Shortly following the declaration that the strait was open, a US official informed Reuters that a military blockade of Iran, involving over 10,000 personnel, remained in effect. Over the weekend, the US Navy fired upon and boarded an Iranian-flagged cargo ship in the Gulf of Oman.

In the US, energy companies reduced the number of operational oil and natural gas rigs for a second consecutive week, marking the first occurrence since March, according to oil technology firm Baker Hughes on Friday.

Note: As of 4 pm EDT 17 April 2026

Currencies

EUR -0.14% to $1.1762

GBP -0.07% to $1.3514

Bitcoin +3.40% to $77,493.56

Ethereum +4.54% to $2,340.21

The US dollar declined to multi-week lows on Friday as investor risk appetite increased following Iran’s announcement that the Strait of Hormuz was open, fuelling optimism that tensions in the Middle East may be easing.

The dollar index ended the session down -0.02% to 98.23, after reaching 97.63 earlier in the day, its lowest point in seven weeks. The dollar index was -0.48% for the week, its second consecutive weekly decline. It has dropped -1.64% since the end of March.

Conversely, the euro strengthened +0.14% to $1.1762, after reaching 1.1848, an eight-week high. The euro rose +0.37% last week, its third straight weekly increase.

Sterling edged -0.07% lower to $1.3514, though it recorded its second consecutive week of gains, advancing +0.42% last week.

The dollar slipped -0.33% to ¥158.61, after previously rising as high as ¥159.86. It followed a -0.43% drop in the previous week, the largest weekly decline in nine weeks.

Fixed Income

US 10-year Bond -6.9 basis points to 4.251%

German 10-year Bund -6.9 basis points to 2.964%

UK 10-year gilt -15.1 basis points to 4.686%

US Treasury yields declined on Friday as growing optimism that the Iran conflict may soon be resolved alleviated concerns about a resurgence in inflation.

The yield on the 2-year note, which closely tracks Fed fund rate expectations, fell -7.4 bps to 3.712%. The yield on the 10-year US Treasury note decreased -6.9 bps to 4.251%, and at the long end, the 30-year yield dropped -2.3 bps to 4.912%.

The spread between 2- and 10-year Treasury yields stood at 53.9 bps, a 0.9 bps increase from the previous week.

Across all maturities, US Treasuries advanced over the past week. The 2-year yield declined -9.8 bps, the 10-year yield fell -8.9 bps and the 30-year yield decreased -0.5 bps.

San Francisco Fed President Mary Daly stated on Friday that businesses remain optimistic the Iran conflict will be brief and that oil prices will not remain elevated for an extended period, although she continues to adopt a cautious ‘wait and see’ approach.

Fed Governor Christopher Waller noted that the Iran conflict could lead to higher inflation in the near term and presents a challenging landscape for monetary policymakers. However, he added that a swift conclusion to the conflict may allow for renewed interest rate cuts later this year.

President Trump’s nominee for Fed Chair, Kevin Warsh, is scheduled for a Senate confirmation hearing on 21 April. If appointed, Warsh is expected to advocate for additional interest rate cuts, succeeding Jerome Powell when his term as chair ends next month.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing in 8.4 bps of rate cuts in 2026, higher than the 5.8 bps priced in a week ago. Fed funds futures traders are now pricing in a 2.1% probability of a 25 bps rate hike at the 29 April FOMC meeting, matching last week’s 2.1% probability.

Eurozone short-term government bond yields declined to one-month lows on Friday, following Iran’s foreign minister’s announcement that all commercial vessels would be permitted passage through the Strait of Hormuz for the duration of the ceasefire.

Money markets reduced expectations for additional ECB rate hikes, now fully pricing in the first increase for July, as opposed to June earlier in the session. The probability of a rate hike at this month’s meeting has been lowered to less than 5%, compared to 15% late Thursday. Market projections now place the ECB’s deposit facility rate at 2.40% by year-end, down from 2.55%, while the current rate remains at 2.00%.

The German two-year Schatz yield, particularly sensitive to changes in interest rate and inflation expectations, fell -11.6 bps to 2.410%, its lowest level since mid-March, resulting in a weekly decrease of -19.9 bps.

Germany’s 10-year government bond yield declined -6.9 bps to 2.964%, totalling a drop of -9.7 bps over the week. At the longer end, the 30-year yield fell -4.9 bps to 3.544%, down -4.3 bps for the week.

Italy’s 10-year government bond yield dropped -11.4 bps to 3.694%, accounting for the majority of last week’s overall -13.6 bps decline. The yield spread between Italian OATs and Bunds narrowed to 73.0 bps, down 3.9 bps from last week’s 76.9 bps.

Note: As of 4 pm EDT 17 April 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.