Higher for how long?

Key data to move markets today

EU: French CPI, Spanish and German Harmonised Index of Consumer Prices, German CPI, Unemployment Change and Rate and Italian CP and GDP

UK: A speech by BoE Governor Andrew Bailey

US: Speeches by Philadelphia Fed President Anna Paulson, San Francisco Fed President Mary Daly and Fed Governor Michelle Bowman

Global Macro Updates

Fedspeak flags upside pressure from energy prices and AI productivity. Fed officials struck a more hawkish tone on Thursday, highlighting upside inflation risks from higher energy prices and the potential productivity effects of artificial intelligence. Speaking at Stanford, Fed Governor Lisa Cook said inflation was moving in the wrong direction and indicated that she would be prepared to raise interest rates if that trend persisted, according to Bloomberg news. At the same time, she said she currently favours keeping policy on hold and expects price pressures to ease in the coming months. She also described the labour market as stable, while noting that downside risks have increased.

Speaking at a BoJ conference, Fed Governor Philiip Jefferson said the current policy stance is well positioned to respond to macroeconomic developments, Bloomberg news reported. He added that inflation should moderate later this year as the effects of tariffs and higher energy costs fade, although he said the balance of inflation risks remains tilted to the upside.

Minneapolis Fed President Neel Kashkari told CNBC that bringing inflation down remains the Fed’s top priority and warned that inflation expectations could become unanchored and move higher. While he did not offer specific guidance on the policy outlook, his remarks followed comments on Wednesday that the Fed could embark on a series of rate increases and that the next policy move could be either a cut or a hike.

According to Reuters, Chicago Fed President Austan Goolsbee said at that same BoJ conference that strong expectations for AI-driven productivity gains could add to inflationary pressures and lead to higher interest rates. He also warned that near-term supply shocks stemming from higher oil prices and supply-chain disruptions could further intensify those pressures.

April core PCE slightly cooler than expected. April core PCE rose 0.24 % m/o/m, below the 0.3 % consensus and the prior 0.30 % increase. On a y/o/y basis, core PCE increased 3.29 %, in line with the 3.3 % consensus and slightly above the prior 3.24 % reading. It also matched November 2023 as the strongest y/o/y print since October 2023.

Personal spending increased 0.5 % m/o/m in April, in line with consensus expectations, while personal income was unchanged, missing the 0.4 % consensus forecast and slowing from the prior 0.6 % increase.

Initial jobless claims for the week ended 23 May rose to 215,000, slightly above the 213,000 consensus and the prior 210,000 reading, which was revised up from 209,000. Continuing claims for the week ended 16 May came in at 1.786 million, modestly below the 1.791 million consensus and up from the prior 1.771 million, which was revised down from 1.782 million.

Headline durable goods orders rose 7.9 % m/o/m in April, well above the 0.8 % consensus, while March was revised up to 1.35 % from 0.85 %. Durable goods orders excluding transportation increased 1.1 %, also ahead of the 0.25 % consensus, with the prior month revised up to 1.1 % from 0.88 %. Core capital goods orders fell 1.1 % after a 3.9 % increase in the previous month, compared with expectations for a 0.4 % m/o/m gain. Core capital goods shipments rose 0.4 % m/o/m, marking a deceleration from the prior 1.3 % increase.

The second estimate of Q1 GDP showed the economy expanding at an annualised rate of 1.6 %, down from the prior 2.0 % reading. The release indicated that the downward revision was driven by weaker investment and consumer spending. Even so, growth remained above the 0.5 % pace recorded in Q4, supported by stronger government spending and investment.

April new home sales totalled 622,000, falling short of the 675,000 consensus and declining 6.2 % from March’s downwardly revised 663,000 pace, previously reported as 682,000. This marked the slowest sales pace since January. Months’ supply rose to 9.4 from 8.7 in March.

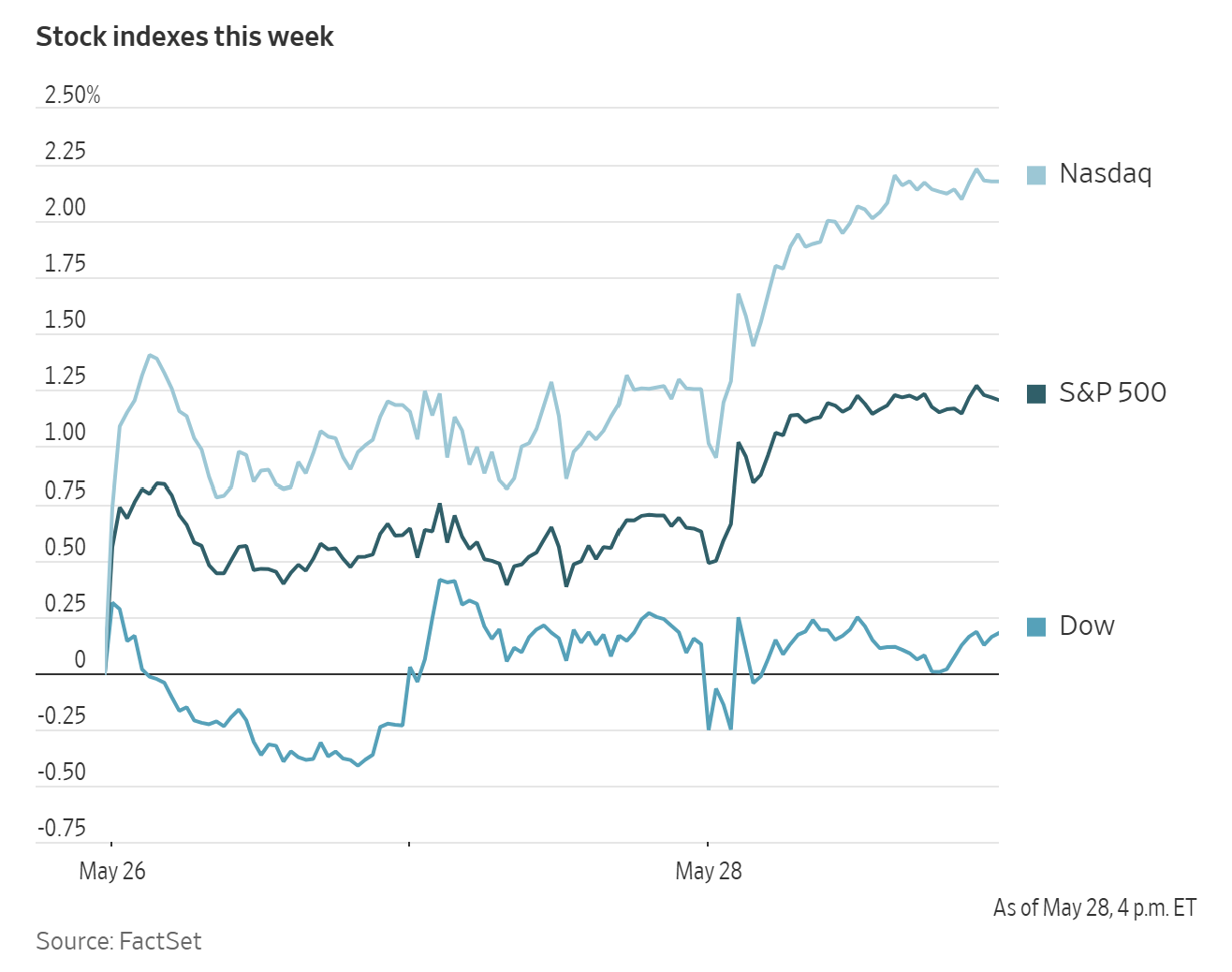

US Stock Indices

Dow Jones Industrial Average +0.05 %

Nasdaq 100 +0.84 %

S&P 500 +0.58 %, with 5 of the 11 sectors of the S&P 500 up

On Thursday, the Nasdaq Composite was +0.91 %, or 242.74 points to 26,917.47 on Thursday. The S&P 500 was +0.58 %, or 43.27 points to 7,563.63. Both indices reached new records, while the S&P 500 notched a six-day winning streak. The Dow Jones was +0.05 %, or 24.69 points higher, to 50,668.97.

In corporate news, Anthropic raised $65 billion in a funding round that valued the artificial intelligence company at $965 billion, including the new capital, surpassing rival OpenAI’s valuation for the first time.

Tilman Fertitta’s long-running effort to acquire Caesars Entertainment culminated in a $5.7 billion all-cash agreement that will add approximately 52 casinos across the US to his entertainment empire.

Shares of Union Pacific and Norfolk Southern declined after a key regulator paused its review of the companies’ proposed $72 billion merger, potentially delaying what would be the largest rail transaction on record.

S&P 500 Best performing sector

Health Care +1.41 %, with Agilent Technologies +16.87%, Charles River Laboratories +10.24% and IQVIA +9.34%

S&P 500 Worst performing sector

Utilities -1.13%, with Xcel Energy -2.15%, Alliant Energy -2.14% and CenterPoint Energy -1.97%

Mega Caps

Alphabet +0.34%, Amazon +0.79%, Apple +0.53%, Meta Platforms +0.01%, Microsoft +3.47%, Nvidia +0.78% and Tesla +0.40%

Information Technology

Best performer: First Solar +10.8%

Worst performer: Synopsys -8.61%

Materials and Mining

Best performer: Freeport-McMoRan +3.52%

Worst performer: Sherwin-Williams -1.56%

European Stock Indices

CAC 40 -0.23%

DAX -0.34%

FTSE 100 -0.75%

Commodities

Gold spot +0.85% to $4,495.03 an ounce

Silver spot +1.38% to $75.64 an ounce

West Texas Intermediate -1.01% to $88.53 a barrel

Brent crude -1.35% to $93.62 a barrel

Gold prices turned higher on Thursday, rising more than 0.8 % after touching a two-month low earlier in the session.

Spot gold climbed +0.85 % to $4,495.03 per ounce after earlier falling to its weakest level since late March.

Data showed that China’s net gold imports through Hong Kong increased 81.2 % in April from the previous month.

Spot silver also rose, gaining +1.38 % to $75.64.

Oil prices settled lower on Thursday after a volatile trading session, as market participants weighed conflicting reports of progress toward a possible agreement to extend the ceasefire between the United States and Iran.

July Brent crude futures, which expire at Friday’s settlement, closed down $1.28, or -1.35 %, at $93.62 per barrel.

US WTI also declined, falling 90 cents, or -1.01 %, to $88.53 per barrel.

Earlier gains were driven by reports that the Islamic Revolutionary Guard Corps had targeted a US airbase overnight, after alleging that the US had struck a site near one of its airbases in southern Iran. The White House later confirmed that it had targeted an Iranian drone operation that posed a threat to a US Navy vessel and a commercial ship in the Strait. In addition, Kuwait’s military reported intercepting several missile and drone threats.

WTI and Brent fell to intraday lows of just below $88 and $93, respectively, after Axios reported that US and Iranian negotiators had reached an agreement on a 60-day memorandum of understanding to extend the ceasefire and begin negotiations on Iran’s nuclear programme. Prices later recovered from those lows because the memorandum had not yet received approval from either President Trump, who was reportedly still considering it, or Iran’s Supreme Leader Ayatollah Ali Khamenei. Iran subsequently denied the report.

The US Department of Energy’s Weekly Petroleum Status Report showed a crude inventory draw of 3.33 million barrels, a gasoline draw of 2.57 million barrels, a distillate draw of 2.11 million barrels and a Cushing draw of 2.8 million barrels, while jet fuel inventories increased by 700,000 barrels.

Refinery crude inputs increased by 652,000 bpd, while net crude imports rose by 360,000 bpd, as the decline in exports more than offset the drop in imports. This was the fifteenth consecutive gasoline draw and the fifth straight week in which jet fuel production remained above 2.0 million bpd.

Cushing inventories have now declined for five consecutive weeks, leaving stockpiles within 3.0 million barrels of operationally critical levels. Refinery utilisation increased by 2.9 percentage points to 94.5 %. Crude, gasoline and distillate inventories are now 2.2 %, 5.6 % and 10.9 % below their respective five-year averages.

Note: As of 4 pm EDT 28 May 2026

Currencies

EUR +0.19% to $1.1648

GBP +0.11% to $1.3442

Bitcoin -0.71% to $73,755.15

Ethereum +0.01% to $2,018.91

The US dollar weakened against major currencies on Thursday. The dollar index declined -0.24 % to 99.00, interrupting a two-session winning streak.

The euro rose +0.19 % against the dollar to $1.1648. The British pound also advanced against the US dollar, rising +0.11 % to $1.3442.

The Japanese yen strengthened +0.14 % against the US dollar to ¥159.21 per dollar. Investors are closely watching whether Japanese authorities will intervene again to support the yen as it trades near the psychologically significant ¥160-per-dollar level.

Fixed Income

US 10-year Bond -3.6 basis points to 4.448%

German 10-year Bund -1.4 basis points to 2.966%

UK 10-year gilt -3.2 basis points to 4.814%

US Treasury yields declined across the curve on Thursday.

A $44 billion auction of seven-year US Treasury notes held in the afternoon drew demand slightly above average, with a bid-to-cover ratio of 2.52x.

The yield on the benchmark 10-year US Treasury note was -3.6 bps at 4.448 %, while the 30-year bond yield fell -3.9 bps to 4.974 %. The two-year US Treasury yield, closely aligned with expectations for the Fed funds rate, fell -0.8 bps to 4.031 %.

The spread between two-year and 10-year US Treasury yields stood at 41.7 bps.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 14.9 bps of rate hikes in 2026, lower than the 20.3 bps priced in a week ago. Fed funds futures traders are now pricing in a 0.9 % probability of a 25 bps rate hike at June’s FOMC meeting, compared to 2.2 % last week.

Eurozone bond yields also declined on Thursday. Money markets slightly pared expectations for additional ECB tightening, although traders continued to price in roughly a 90 % probability of a rate increase next month. Markets were also pricing in about 55 bps of tightening over the remainder of the year.

Eurozone bond yields have risen sharply since the war began on 28 February, as traders increasingly expect the ECB to deliver as much as 75 bps of tightening, equivalent to three full rate increases, to counter inflation driven by higher oil prices resulting from the Iran war.

Germany’s 10-year bond yield fell -1.4 bps to 2.966 % on Thursday. Germany’s two-year bond yield, sensitive to expectations for the ECB deposit rate, fell -3.6 bps to 2.561 %, while the 30-year yield declined -1.7 bps to 3.518 %.

The 10-year Italian BTP yield was unchanged at 3.695 %, leaving the spread over German Bunds at 72.9 bps.

Note: As of 4 pm EDT 28 May 2026

DISCLAIMER: This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.