Fiscal ambition under monetary restraint?

Key data to move markets today

EU: French, German and Eurozone HCOB Composite, Manufacturing and Services PMIs and speeches by Banco de España Governor José Luis Escrivá and ECB’s Chief Economist Philip Lane, Vice President Boris Vujčić and Executive Board Member Frank Elderson

UK: S&P Global Composite, Manufacturing and Services PMIs and speeches by BoE External Members Alan Taylor and Swati Dhingra

USA: ADP Employment Change 4-week Average and S&P Global Composite, Manufacturing and Services PMIs

Global Macro Updates

ECB President Lagarde downplays the risk of second-round effects. In remarks to the Hearing of the Committee on Economic and Monetary Affairs of the European Parliament, ECB President Lagarde downplayed the risk of second-round effects from the energy price surge from the war with Iran, noting that there is no evidence that inflation expectations have become de-anchored in a way that would require a more aggressive policy response.

Recent remarks from ECB officials suggest that policymakers remain inclined toward one additional rate increase, although a move in July appears unlikely. Sell-side economists expect a precautionary increase in September, when updated macroeconomic projections should provide greater clarity and make the decision easier to communicate.

Bloomberg news noted that eurozone interest rate markets are pricing in roughly 33 bps of tightening by year-end. While some hawkish officials argue that the Iran deal is unlikely to materially reduce inflation pressures already moving through the economy, more dovish officials remain concerned about the risk of overtightening as growth slows. Recent wage indicators have moderated and labour market conditions are beginning to soften.

The policy debate increasingly appears to be shifting away from whether inflation will reaccelerate and toward how much additional restraint is needed to ensure inflation continues moving sustainably toward target.

Andy Burnham’s path toward becoming the next UK prime minister. Sell-side economists broadly view the UK political transition as orderly rather than a systemic shock. Markets appear to have absorbed most of the immediate political risk following Sir Keir Starmer’s resignation as UK prime minister and Labour leader, as well as Andy Burnham’s emergence as the frontrunner. SEB and ING noted only modest moves in UK assets, suggesting a contained political risk premium rather than disorderly repricing.

Economists at Pantheon Macroeconomics emphasise that fiscal credibility, rather than the leadership change itself, remains the central market driver. The key pricing question is whether Burnham anchors policy to the existing fiscal rules or shifts toward a looser fiscal stance, including higher spending, welfare expansion and regional investment.

Analysts regard the choice of chancellor as the most important initial signal. Retaining Chancellor Rachel Reeves, or appointing a similarly fiscally-inclined figure, would likely anchor Gilts and GBP. By contrast, a replacement perceived as fiscally expansionary could trigger renewed risk premia and become the most important near-term market catalyst.

Burnham’s fiscal stance is generally viewed as having an expansionary bias, although it would remain constrained by high debt, at around 100% of GDP, and elevated debt-servicing costs. Analysts expect a policy tilt toward higher spending on welfare, infrastructure and regional growth programmes, alongside potential tax increases, including wealth and income taxes.

Fiscal rules are more likely to be reinterpreted than abandoned. Pantheon argues that past experience suggests fiscal frameworks can be flexible, with risks skewed toward shifting the time horizon for borrowing targets, such as five-year targets, to allow near-term stimulus while deferring consolidation.

The consensus sell-side view points to modest upward pressure on gilt yields over the medium term, with GBP likely to remain range-bound, but skewed to the downside. Market attention is expected to remain focused on fiscal signalling through early cabinet appointments rather than the leadership change itself, while volatility is likely to remain event-driven rather than structural.

Equity implications are viewed as mixed, with domestically oriented sectors most exposed. Analysts highlight the risk that higher taxes, tighter labour regulation or public ownership concerns could weigh on UK equities, particularly domestic names. However, infrastructure- and housing-linked sectors could benefit from a more pro-growth policy agenda.

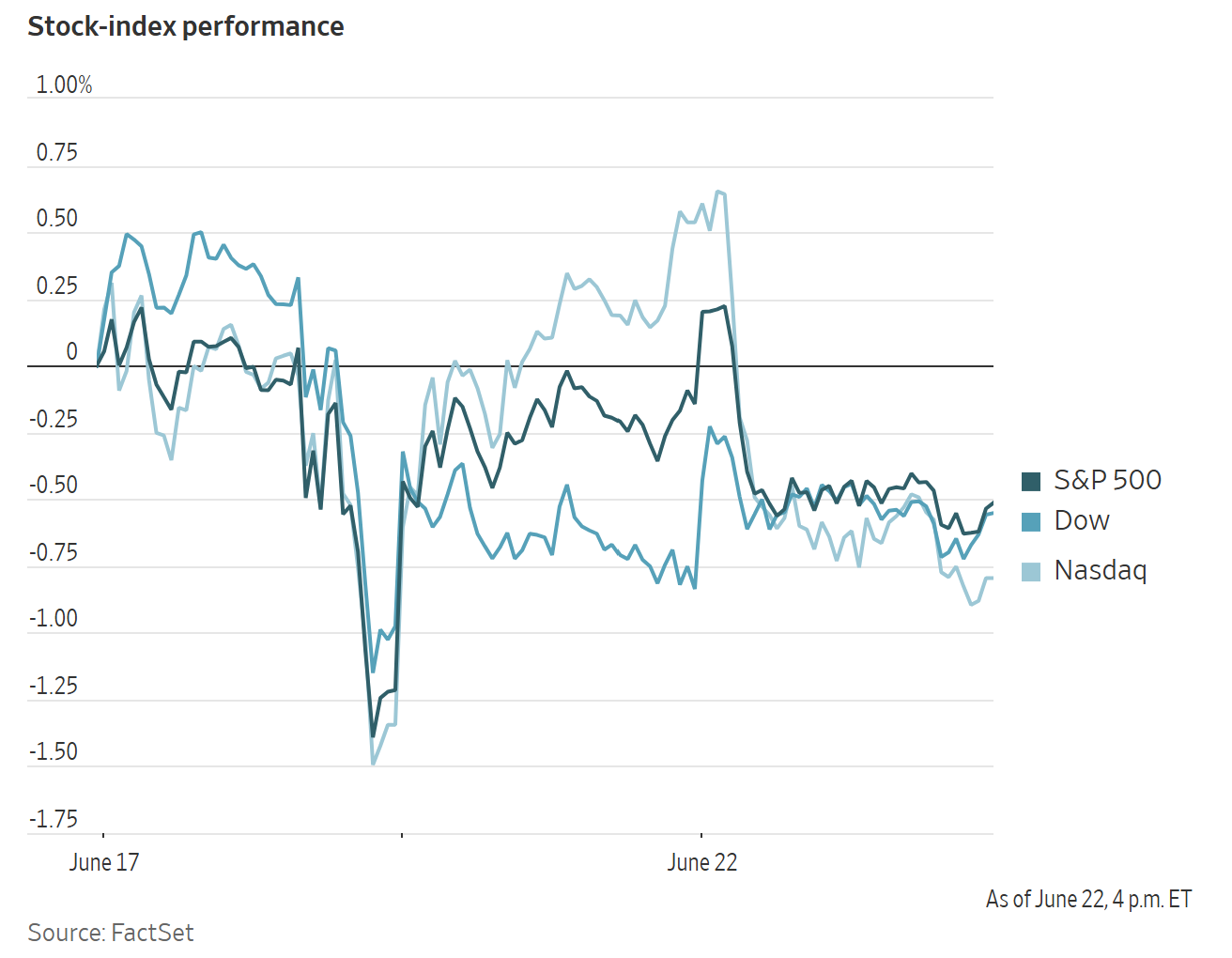

US Stock Indices

Dow Jones Industrial Average +0.29%

Nasdaq 100 -0.19%

S&P 500 -0.37%, with 4 of the 11 sectors of the S&P 500 down

US equities retreated from near-record highs as weakness among several large technology companies outweighed optimism around progress in peace talks between the US and Iran.

On Monday, the S&P 500 lost -0.37%. The Dow Jones Industrial Average added +0.29%, or 148.01 points. The Nasdaq Composite declined by -1.32%.

In corporate news, Alphabet shares declined after Google DeepMind Vice President John Jumper, who won the 2024 Nobel Prize in chemistry for his work on AI, announced that he would leave the company to join Anthropic PBC.

Definium Therapeutics shares surged on Monday after the biotechnology company reported that a single dose of its LSD-based drug, DT120, significantly reduced depression symptoms in a late-stage trial. The treatment outperformed placebo by 8.1 points on a 60-point physician-administered depression scale six weeks after dosing, with the benefit sustained at the three-month mark.

Domino’s Pizza appointed COO Joe Jordan, 53, as its next chief executive, effective 1 October. Current CEO Russell Weiner will move to executive chairman and is expected to fully assume that role next year.

AbbVie agreed to acquire Apogee Therapeutics for $10.9 billion as part of an effort to strengthen its core immunology franchise. The transaction includes Apogee’s experimental drug zumilokibart, a potential competitor to Dupixent for moderate to severe atopic dermatitis. AbbVie said it would pay $135.11 per share in cash, representing a 49% premium to Apogee Therapeutics’ Thursday closing price of $90.38. The acquisition is expected to close in Q3 and reduce adjusted EPS by 46 cents in 2027.

EasyJet’s board rejected Castlelake’s third £4.74 billion takeover proposal, while the US firm urged shareholders to support the offer. The board said the bid fundamentally undervalued the airline and was opportunistically timed, given the temporary pressure on easyJet’s shares from the Middle East conflict. Castlelake’s offer of 625 pence per share represents a 59% premium to the 28 May closing price of 394.20 pence. Under the proposal, the bidding vehicle would be owned 49% by Castlelake and 51% by EU nationals, and potentially other investors, to comply with EU ownership rules.

SpaceX lost $400 bn in market value on Monday, ending down 16.4% at $154.60, 31.5% below the IPO high on 11 June. The drop was due to the reversal in bond yields, following increasing expectations of a Fed rate rise. As noted by the Financial Times analysis of Bloomberg data, the $400 bn hit to SpaceX’s market capitalisation ranks as the second-biggest one-day loss suffered by any company. SpaceX ended the session with a market cap of $2.03 tn, down from an intraday peak of almost $3 tn on 16 June.

S&P 500 Best performing sector

Real Estate +1.38%, with Digital Realty Trust +3.93%, Iron Mountain +3.15% and Prologis +2.34%

S&P 500 Worst performing sector

Communication Services -3.83%, with Netflix -5.82%, Fox -5.44% and Alphabet -5.08%

Mega Caps

Alphabet -5.08%, Amazon -4.75%, Apple -0.34%, Meta Platforms -2.32%, Microsoft -3.18%, Nvidia -0.97% and Tesla +1.14%

Information Technology

Best performer: Super Micro Computer +15.66%

Worst performer: Palantir Technologies -6.98%

Materials and Mining

Best performer: Smurfit Westrock +2.69%

Worst performer: FMC -4.50%

European Stock Indices

CAC 40 -0.25%

DAX +0.62%

FTSE 100 +0.72%

Commodities

Gold spot +0.86% to $4,190.43 an ounce

Silver spot +0.00% to $64.90 an ounce

West Texas Intermediate -4.14% to $74.33 a barrel

Brent crude -2.99% to $77.98 a barrel

Gold strengthened on Monday, recovering from a more than one-week low reached in the previous session.

Spot gold rose +0.86% to $4,190.43 per ounce after touching its lowest level since 11 June on Friday, while spot silver was unchanged at $64.90 per ounce.

Oil prices settled more than two percent lower on Monday as supply concerns eased. The decline followed comments from US Vice President JD Vance that progress had been made in talks with Iran and that the Strait of Hormuz remained open.

Brent crude settled down $2.40, or -2.99%, at $77.98 a barrel. Earlier in the session, prices had risen to $82.30 after threats by the US President to restart the Iran war and Tehran’s announcement that it had again closed the Strait. US WTI settled $3.21 lower, or -4.14%, at $74.33.

High-ranking US and Iranian officials concluded their first round of talks in Switzerland on Monday, according to mediators. The discussions began on Sunday under a memorandum of understanding reached last week to extend a fragile April ceasefire for at least another 60 days.

Iran did not negotiate on its nuclear programme and did not accept any new commitments during Sunday’s talks with the US in Switzerland, Foreign Ministry spokesperson Esmaeil Baghaei told the official IRNA news agency.

Tensions had escalated over the weekend after Iran threatened to block the Strait if Israel did not stop attacks against Lebanon, while Trump countered with a threat to restart the war. Those concerns eased after reports of progress at the Switzerland talks. Shortly after 9:00 ET, Treasury Secretary Bessant issued a temporary 60-day general licence authorising Iranian production and sales through 21 August.

Iran’s top negotiator, Mohammad Baqetr Qalibaf, travelled to Oman to discuss arrangements for managing Strait of Hormuz traffic. Technical talks between US and Iranian officials continued in Switzerland, while Secretary of State Rubio was scheduled to meet Gulf Arab allies on Tuesday to discuss the agreement. Key concerns among those allies include Iran’s ballistic missile programme and the possibility that a $300 billion reconstruction fund could be used to rebuild Iran’s military capacity.

Tanker data indicated an acceleration of traffic through the Strait in recent days. Trading sources also said Iraq, the UAE and Kuwait were selling additional spot oil cargoes into the market.

KSA crude inventories fell to 139.967 million barrels from 152.645 million in March. Direct crude burn rose to 540,000 bpd from 330,000 bpd, while crude exports averaged 3.986 million bpd, down from 4.974 million bpd. Combined crude and product exports averaged 4.995 million bpd, compared with 6.131 million bpd in March.

In Russia, Deputy Prime Minister and former Energy Minister Alexander Novak said the government was preparing measures to address domestic fuel shortages caused by continued Ukrainian strikes on Russian refineries.

Iraq plans to restore crude production gradually to between 4.2 million and 4.3 million bpd, according to its deputy oil minister for upstream affairs.

Note: As of 4 pm EDT 22 June 2026

Currencies

EUR -0.36% to $1.1427

GBP +0.10% to $1.3245

Bitcoin +1.72% to $64,247.49

Ethereum +1.55% to $1,730.98

The dollar advanced on Monday, while sterling traded higher in volatile conditions after British Prime Minister Keir Starmer announced his resignation.

The dollar index rose +0.23% to 101.00, while the euro declined -0.36% to $1.1427.

Sterling recovered from a session low of $1.3175 after Starmer’s resignation announcement opened the possibility that rival Andy Burnham could become the country’s seventh prime minister in ten years as soon as next month. Sterling was up +0.10% on the day at $1.3245.

Against the Japanese yen, the dollar strengthened +0.16% to ¥161.54 after reaching ¥161.92, just shy of last week’s two-year high. A break above ¥161.96 would leave the yen at its weakest level since 1986.

The Japanese currency experienced several sharp intraday moves, briefly strengthening against the greenback.

Following the BoJ’s widely expected rate increase last week, Japanese Finance Minister Satsuki Katayama said authorities were prepared to respond appropriately to currency moves at any time.

Fixed Income

US 10-year Bond +5.6 basis points to 4.516%

German 10-year Bund -3.2 basis points to 2.960%

UK 10-year Gilt -3.0 basis points to 4.816%

US Treasury yields rose across the curve on Monday, with the rate-sensitive 2-year yield reaching a 16-month high.

The 2-year note yield, which typically tracks Fed funds rate expectations, increased +5.2 bps to 4.239%, its highest level since February 2025.

The yield on the US 10-year note rose +5.6 bps to 4.516%. At the long-end of the curve, the 30-year yield advanced by +5.2 bps to 4.950%.

The spread between 2-year and 10-year notes steepened slightly, widening 0.4 bps to 27.7 bps after reaching 24.2 bps on Thursday, its flattest level since March 2025.

The return to a Greenspan-style toolkit, characterised by brief statements, limited guidance and a smaller balance sheet, could result in a noisier front end and a more volatile curve shape, even if the overall level remains flat.

The highlight of this week’s US economic calendar will be Thursday’s PCE inflation report. Core prices are expected to have risen 0.3% in May, lifting the annual rate to 3.4%, while headline inflation is forecast at 0.5% for the month and 4.1% y/o/y.

On the supply front, the Treasury will auction $183 billion of short- and intermediate-term coupon-bearing notes this week, including $69 billion in 2-year notes on Tuesday, $70 billion in 5-year notes on Wednesday and $44 billion in 7-year notes on Thursday.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 40.7 bps of rate hikes in 2026, higher than the 18.5 bps priced in a week ago. Fed funds futures traders are now pricing in a 34.2% probability of a 25 bps rate hike at July’s FOMC meeting, compared to 6.4% last week.

Eurozone government bond yields declined across regions and maturities on Monday.

Germany’s 10-year bond yield fell -3.2 bps to 2.960%.

The ECB became the first major central bank to raise interest rates since the conflict began earlier in June, seeking to curb inflation before higher energy costs spread more broadly through the economy.

On Monday, markets slightly reduced expectations for tightening by year-end, with futures pricing in about 31 bps of rate increases, down from around 35 bps at Friday’s close.

After the ECB’s 11 June rate increase, markets had priced in about 40 bps of tightening by the December policy meeting.

Germany’s 2-year yield, which is sensitive to changes in ECB rate expectations, fell -4.8 bps to 2.638%. At the long end of the maturity spectrum, the 30-year yield declined -2.3 bps to 3.513%.

Investors were also monitoring potential spillover from Britain after Prime Minister Keir Starmer announced his intention to resign. This paved the way for Andy Burnham, the former mayor of Greater Manchester and now a member of parliament (MP), who is expected to be more open to looser fiscal policy than Starmer, to become prime minister.

Britain’s 10-year gilt yield fell -3.0 bps to 4.816% after Wes Streeting, another expected leadership candidate, said he would support Burnham for prime minister.

On the periphery, Italy’s 10-year BTP yield declined -3.9 bps to 3.658%, leaving the spread over Bunds at 69.8 bps.

Note: As of 4 pm EDT 22 June 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.