Is Big Tech rotation powering semis and cyclicals?

Key data to move markets today

EU: Spanish Harmonised Index of Consumer Prices, Eurozone Business Climate, Consumer Confidence and Economic Sentiment Indicator Surveys and a speech by ECB President Christine Lagarde

Global Macro Updates

Potential OpenAI IPO delay and Big Tech rotation in focus. OpenAI is reportedly considering delaying its IPO until 2027 amid uncertain market conditions, according to The New York Times. The company had initially targeted a $1 tn valuation, but advisers warned that level may be difficult to achieve in the current environment, citing SpaceX’s weak post-IPO stock performance. CEO Altman is reportedly unwilling to reduce the valuation target.

The overlap between AI and politics is also back in focus after the Trump administration reportedly asked OpenAI to stagger the release of its upcoming GPT-5.6 model. The report follows recent White House restrictions on Anthropic and adds to broader concerns around open source, competition from Chinese models and the risk of reliance on a single AI provider.

Thursday’s weakness in Big Tech was partly attributed to demand destruction, price increases and questions over memory-driven gross-margin sustainability following Micron’s results. At the same time, competition and supply dynamics remain in focus, with Samsung and SK Hynix announcing, according to the Financial Times, that they will invest a combined $590 bn alongside the South Korean government to build chipmaking facilities in under-developed parts of South Korea.

Rotation remains a key theme, with Big Tech serving as a source of funds for moves into semiconductors and memory. Markets appear underweight ‘buyers of shortage,’ or companies with high CapEx and multi-year ROI profiles, versus ‘sellers of shortage,’ which benefit from one-time sales and near-term EPS revisions. BofA analysts noted that liquidity has shifted from megacap AI arms-race names into semiconductors and illiquid cyclicals, including housing and REITs, as investors position ahead of a potential Trump affordability pivot.

US consumer sentiment improves. Final June Consumer Sentiment rose to 49.5, below the 50.0 consensus but above May’s final reading of 44.8, which marked a record low. May’s weakness was driven by a sharp rise in gasoline prices tied to the Iran conflict, while concerns eased in early June as fuel prices moderated.

One-year inflation expectations edged down to 4.6% from 4.8% in May, though they remain above February’s pre-conflict level of 3.4%. Long-run inflation expectations fell to 3.3% from 3.9%.

The Current Economic Conditions Index improved to 47.7 from 45.8 in May, while the Index of Consumer Expectations rose to 50.7 from 44.1.

The report said sentiment improved broadly as concerns over the long-term effects of the Iran conflict eased, though overall confidence remains weak as high prices continue to pressure household finances.

The consumer sector has been a market bright spot this month, supported by the sharp pullback in oil prices.

US Stock Indices

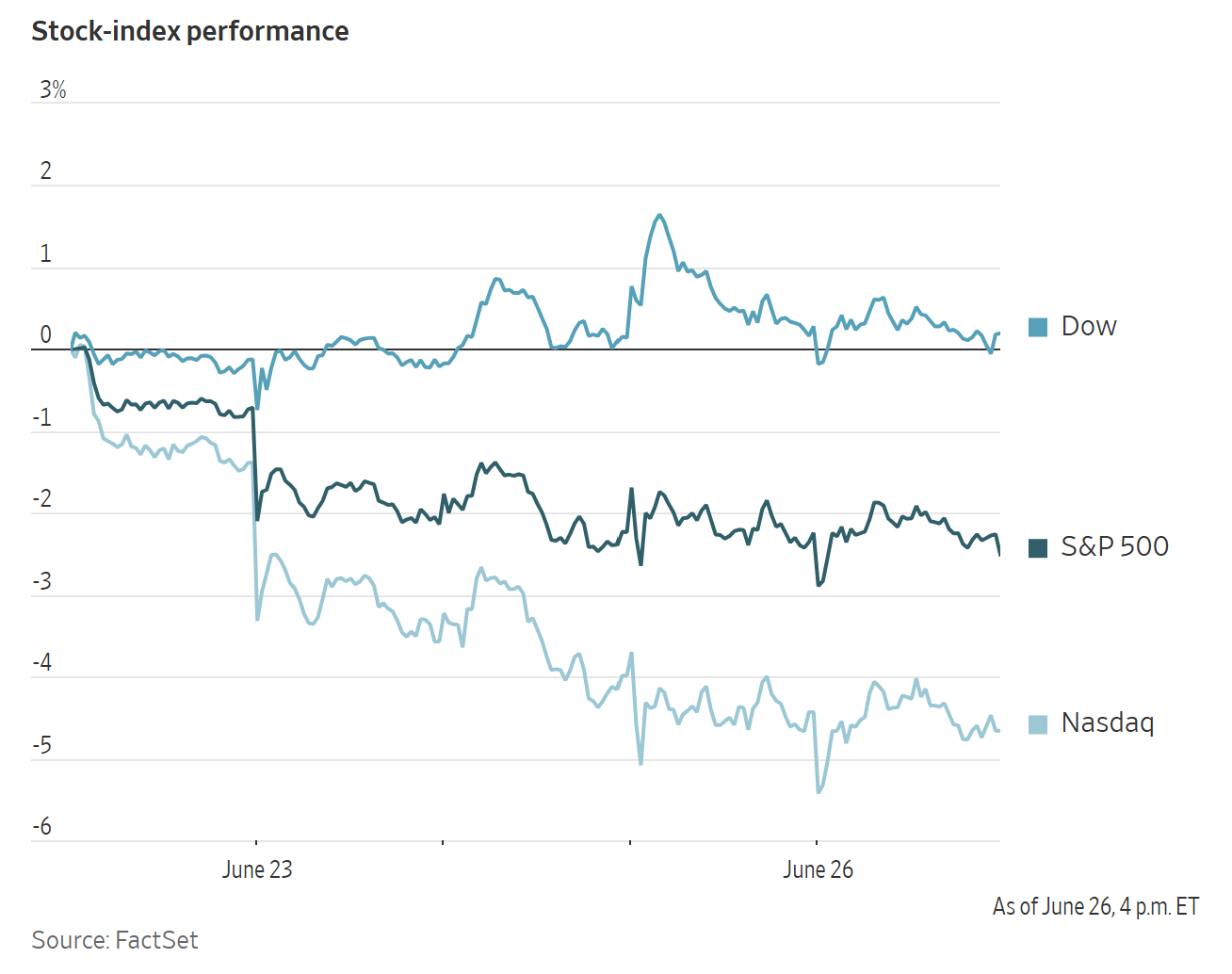

Dow Jones Industrial Average -0.09%

Nasdaq 100 -1.09%

S&P 500 -0.05%, with 5 of the 11 sectors of the S&P 500 down

Concerns over AI, private credit, war-related supply-chain disruptions and elevated interest rates have created renewed headwinds for the stock-market rally.

The Nasdaq Composite fell -0.24%, the S&P 500 slipped -0.05% and the Dow Jones Industrial Average declined -0.09%, or 44.51 points.

Stocks ended Friday with a fifth straight daily decline, as even strong earnings from chip maker Micron failed to lift major indexes. The S&P 500 and Nasdaq Composite each fell every day of the week for the first time since April 2024, losing -1.59% and -3.32%, respectively. The Dow Jones finished the week +0.32% higher.

In corporate news, ON Semiconductor agreed to acquire Synaptics in an approximately $7 billion all-stock deal aimed at expanding its presence in physical AI. ON Semiconductor said it will issue 1.35 shares for each Synaptics share, representing about a 19% premium to the two companies’ volume-weighted average prices over the past 10 trading days. One Synaptics board member will join ON Semiconductor’s board. The transaction is expected to close by mid-next year.

Eli Lilly said European regulators issued a positive opinion recommending Jaypirca for chronic lymphocytic leukemia.

NASA selected Rocket Lab to launch two missions using its Electron rocket.

Zalando shares fell in European trading after Germany’s financial regulator opened an audit of the company’s financial statements, alleging that a transaction tied to its acquisition of About You may have been omitted.

S&P 500 Best performing sector

Health Care +3.16%, with Moderna +12.59%, Eli Lily +7.13% and Biogen +6.97%

S&P 500 Worst performing sector

Industrials -1.53%, with Cummins -5.73%, Caterpillar -5.63% and Generac Holdings -5.60%

Mega Caps

Alphabet -2.19%, Amazon +2.50%, Apple +3.14%, Meta Platforms +1.36%, Microsoft +5.71%, Nvidia -1.64% and Tesla +1.22%

Information Technology

Best performer: ServiceNow +85%

Worst performer: ON Semiconductor -23.66%

Materials and Mining

Best performer: FMC +3.80%

Worst performer: Albemarle -5.21%

European Stock Indices

CAC 40 -0.55%

DAX -1.29%

FTSE 100 -0.21%

Commodities

Gold spot +1.55% to $4,088.23 an ounce

Silver spot +2.23% to $59.16 an ounce

West Texas Intermediate -2.06% to $70.00 a barrel

Brent crude -2.36% to $72.93 a barrel

Gold rose on Friday, but ended the week lower.

Spot gold rose +1.55% to $4,088.23 per ounce. The softer US dollar improved the relative appeal of dollar-priced bullion for overseas buyers.

On a weekly basis, gold prices declined -1.60%.

Spot silver also advanced, gaining +2.23% to $59.16 per ounce. However, spot silver fell -8.84% throughout the week.

Oil prices rose more than two percent on Thursday as renewed security concerns around the Strait of Hormuz revived worries over global crude flows.

Brent futures declined $1.76, or -2.36%, to settle at $72.93 per barrel, while US WTI crude advanced $1.47, or -2.06%, to settle at $70.00.

WTI and Brent have retraced to pre-war levels as tanker traffic through the Strait of Hormuz normalises, regional production begins to return online and Chinese demand remains subdued. The US lifted the blockade and targeted sanctions on Iranian oil last week. Tanker flows through the Strait have increased from already elevated levels following the MOU signing. Iran’s warning against vessels that do not coordinate Strait crossings, along with a subsequent attack on a container ship, briefly slowed volumes on Thursday. However, traffic has since recovered, with at least 37 ships transiting the Strait since the vessel was hit.

Gulf countries are restarting production, reopening export facilities, issuing their first crude tender offers since the war began or increasing the number of offers from last week. Markets have largely discounted comments from Iran and Oman suggesting that shippers may face a fee to transit the Strait of Hormuz; Oman reportedly raised that possibility with European allies on Friday.

The elevated pace of Ukrainian attacks on Russian energy infrastructure seen in May has carried into June, with at least five refineries, as well as oil and fuel depots, targeted last week. The 260,000 bpd Moscow refinery, which was hit twice the prior week, is expected to remain offline for at least six months.

Fuel shortages in Russia are widening, with hundreds of cars reportedly queued for gasoline at stations across the country. Deputy Prime Minister Novak said Russia is considering a ban on diesel exports and is seeking to import gasoline from Kazakhstan. Diesel futures in the US and elsewhere received support following the initial report, with Russian diesel export capacity exceeding 900,000 bpd. Multi-year-low refinery utilisation has also pushed Russian seaborne crude exports to year-to-date highs.

China’s demand remains weak. Tanker data indicate that China’s crude imports this month are tracking near the multi-year lows reached in May, while traders said Chinese companies are reselling West African cargoes. Teapot refinery utilisation is at nine-year lows. China is allowing state-owned refineries to increase fuel exports next month.

Iraq said it is pressing OPEC to raise its production quota, while denying a Reuters report that it is considering leaving the group. The Department of Energy Weekly Petroleum Status Report marked another large combined commercial and SPR crude draw of more than 15 million barrels. Cushing inventories fell firmly into operationally critical levels, while distillate and gasoline stocks each built by 3.06 million barrels. Jet fuel production remained above 2.0 million bpd for an eighth consecutive week. Total crude inventories, including commercial and SPR stocks, are at more than 42-year lows, while product inventories at Fujairah and Singapore each rose by more than 6.0 million barrels w/o/w.

Note: As of 4 pm EDT 26 June 2026

Currencies

EUR +0.10% to $1.1383

GBP +0.05% to $1.3200

Bitcoin -1.10% to $59,864.51

Ethereum -2.02% to $1,573.38

The US dollar was on the defensive on Friday, although it remained on track for its largest monthly gain in nearly a year.

The euro was +0.10% higher at $1.1383 after touching a 13-month low against the dollar last week. It still recorded a weekly decline of -0.74%. Sterling traded +0.05% higher at $1.3200 and was down -0.24% for the week.

The Japanese yen traded -0.02% lower at ¥161.73, remaining near a 40-year low. Over the week, the yen depreciated -0.28% against the US dollar.

The dollar index was marginally lower, down -0.06% at 101.37 on Friday, after advancing +0.60% over the week.

Investors are now focussed on this week’s US non-farm payrolls and unemployment data, which could provide fresh insight into labour market strength and the outlook for Fed policy.

The ECB’s annual forum will also be closely watched this week as investors assess the evolution of central bank policy amid lower oil prices and continued equity-market volatility.

ECB President Christine Lagarde opens the forum on Monday, followed by a key policy panel on Wednesday featuring Fed Chair Warsh, as markets seek a clearer read on the new Fed chief.

Fixed Income

US 10-year Bond -0.8 basis points to 4.387%

German 10-year Bund -0.5 basis points to 2.856%

UK 10-year Gilt +3.2 basis points to 4.738%

Short-dated US Treasury yields declined on Friday.

The 2-year note yield, which typically tracks Fed rate expectations, fell -1.8 bps to 4.117%, its lowest level since 17 June.

The yield on US 10-year notes declined -0.8 bps to 4.387%.

The 2s10s curve steepened by 1.0 bps to 27.0 bps. At the long end of the curve, the 30-year yield rose 0.3 bps to 4.868%.

For the week, yields declined across the curve. The 2-year yield fell -7.0 bps, the 10-year yield traded -7.3 bps lower, and the 30-year yield ended -3.0 bps lower.

The June employment report is due on 2 July and is expected to show that employers added 110,000 jobs during the month.

According to CME Group's FedWatch Tool, Fed funds futures traders are pricing 32.8 bps of rate hikes in 2026, lower than the 38.6 bps priced in a week ago. Fed funds futures traders are now pricing in a 29.4% probability of a 25 bps rate hike at July’s FOMC meeting, compared to 38.5% last week.

Eurozone bond yields edged lower on Friday and recorded their largest weekly decline in more than a year after an ECB survey showed that consumers reduced their near-term inflation expectations in May.

Germany’s 10-year bond yield fell -0.5 bps to 2.856%, its lowest level since mid-March. The yield declined -13.6 bps last week, marking the largest weekly drop since March 2025.

Germany’s 2-year bond yield, which is sensitive to rate expectations, was down -0.9 bps at 2.526%, after falling to its lowest level since early May. At the long end of the German curve, the 30-year yield traded +0.7 bps higher at 3.411%.

ECB Governing Council member Isabel Schnabel said on Thursday that the ECB will need to continue raising interest rates following its earlier June hike.

Money-market traders on Friday priced in 24 bps of additional ECB tightening this year, implying that another hike remains likely, though expectations have declined from 37 bps on Monday.

For the week, the German curve shifted lower. The 2-year Schatz yield declined -13.9 bps, the 10-year yield fell -13.6 bps, and the 30-year yield ended the week -12.5 bps lower.

Italy’s 10-year BTP yield traded -1.3 bps lower on Friday to 3.585%, leaving the spread over Bunds at 72.9 bps. Italy’s 10-year yield declined -11.2 bps through the course of the week.

Note: As of 4 pm EDT 26 June 2026

While every effort has been made to verify the accuracy of this information, EXT Ltd. (hereafter known as “EXANTE”) cannot accept any responsibility or liability for reliance by any person on this publication or any of the information, opinions, or conclusions contained in this publication. The findings and views expressed in this publication do not necessarily reflect the views of EXANTE. Any action taken upon the information contained in this publication is strictly at your own risk. EXANTE will not be liable for any loss or damage in connection with this publication.

This article is provided to you for informational purposes only and should not be regarded as an offer or solicitation of an offer to buy or sell any investments or related services that may be referenced here. Trading financial instruments involves significant risk of loss and may not be suitable for all investors. Past performance is not a reliable indicator of future performance.

Created by professionals. For professionals.